Editor’s Note: this report was updated on Sept. 13, 2018, after the original publication with revised loan origination data. For more details on the revisions contact christine.stricker@attomdata.com.

IRVINE, Calif. – Sept. 13, 2018 — ATTOM Data Solutions, curator of the nation’s premier property database, today released its Q2 2018 U.S. Residential Property Loan Origination Report, which shows that more than 2 million (2,087,455) loans secured by residential property (1 to 4 units) were originated in Q2 2018, up 15 percent from the previous quarter and up less than 1 percent from a year ago.

- 926,516 of the residential loans originated in Q2 2018 were purchase loans, up 39 percent from the previous quarter and up 1 percent from a year ago.

- 799,093 of the residential loans originated in Q2 2018 were refinance loans, down less than 1 percent from the previous quarter and down 2 percent from a year ago to the lowest level since Q1 2014, a nearly four-year low.

- 361,845 Home Equity Lines of Credit (HELOCs) were originated on residential properties in Q2 2018, up 4 percent from the previous quarter and up 2 percent from a year ago to the highest level since Q3 2008, a nearly 10-year high.

The loan origination report is derived from publicly recorded mortgages and deeds of trust collected by ATTOM Data Solutions in more than 1,700 counties accounting for more than 87 percent of the U.S. population. Counts and dollar volumes for the two most recent quarters are projected based on available data at the time of the report (see full methodology below).

“Rising mortgage rates are continuing to cool demand for refinance originations, which were down to their lowest level since 2014 — the last time we saw more than six consecutive months with average 30-year fixed mortgage rates above 4 percent,” said Daren Blomquist, senior vice president at ATTOM Data Solutions. “Meanwhile buyers are upping the ante when it comes to down payments, evidenced by the record-high median down payment for homes purchased in the quarter, and an increasing number of buyers are getting help from co-buyers.”

Markets with decreasing refi originations led by Los Angeles, Chicago, Philadelphia

Ninety-nine of the 173 metropolitan statistical areas analyzed in the report (57 percent) posted a year-over-year decrease in refinance originations in Q2 2018, including Los Angeles, California (down 13 percent); Chicago, Illinois (down 5 percent); Philadelphia, Pennsylvania (down 9 percent); Washington, D.C. (down 21 percent); and Atlanta, Georgia (down 12 percent).

“In the current market environment of rising interest rates and lower loan volumes, it is more important than ever for mortgage lenders to seek out innovative ways to reduce costs, accelerate loan cycle times and provide a best-in-class consumer experience,” said Paul Doman, president and CEO of Accurate Group, which provides appraisal management and title services to lenders. “The lenders who are faring the best in terms of efficiency and borrower satisfaction are those that have kept pace with and implemented new technologies across multiple facets of the loan process.”

Counter to the national trend, 74 of the 173 metropolitan statistical areas analyzed in the report (43 percent) posted a year-over-year increase in refinance originations in Q2 2018, including New York, New York (up 17 percent); Dallas-Fort Worth, Texas (up 15 percent); Houston, Texas (up 69 percent); Miami, Florida (up 31 percent); and Boston, Massachusetts (up 23 percent).

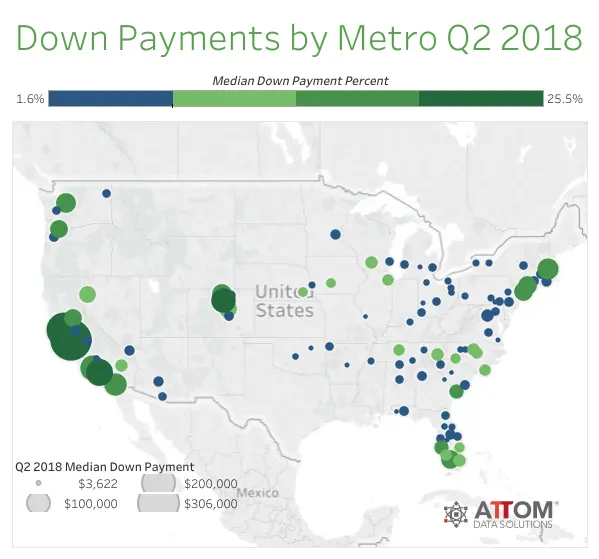

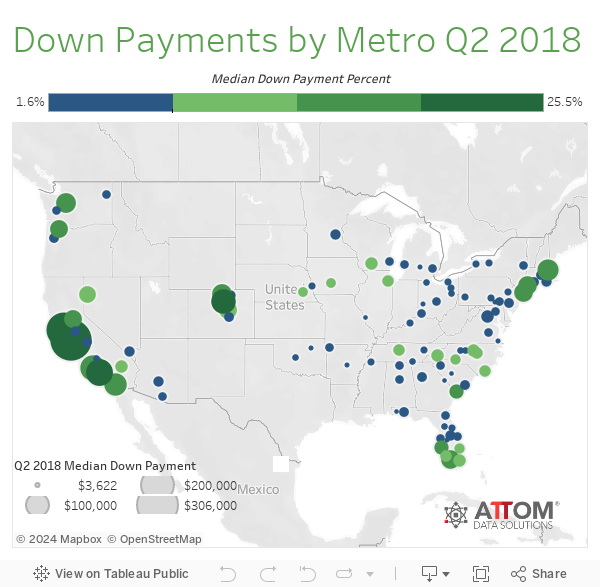

Median down payment increases to new record high

The median down payment on single family homes and condos purchased with financing in Q2 2018 was $19,900, up 19 percent from $16,750 in the previous quarter and up 18 percent from $16,925 in Q2 2017 to a new record high going back as far data is available — Q1 2000.

The median down payment of $19,900 was 7.6 percent of the median sales price of the homes purchased with financing during the quarter, up from 6.6 percent in the previous quarter and up from 6.6 percent in Q2 2017 to the highest level since Q3 2003 — a nearly 15-year high.

Among 103 metropolitan statistical areas analyzed for median down payments, those with the biggest median down payments for homes purchased in Q2 2018 were San Jose, California ($306,000); San Francisco, California ($220,000); Los Angeles, California ($130,000); Oxnard-Thousand Oaks-Ventura, California ($115,400); and Boulder, Colorado ($107,750).

Other metro areas with median down payments of $60,000 or higher in the second quarter were San Diego, California ($90,400); Boston, Massachusetts ($79,925); Seattle, Washington ($70,100); Fort Collins, Colorado ($68,050); Bridgeport, Connecticut ($63,550); New York, New York ($62,108); and Naples, Florida ($60,000).

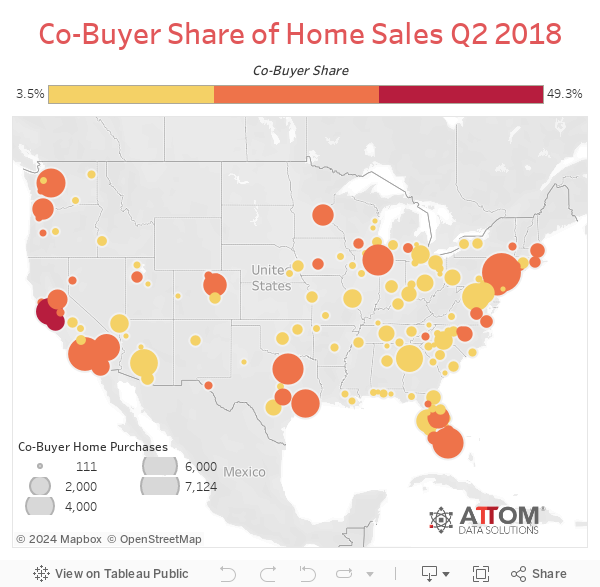

Co-buyers account for 17.6 percent of all Q2 2018 home sales

Nationwide, 17.6 percent of all single family home purchases in Q2 2018 were to co-buyers (multiple, non-married buyers listed on the sales deed), up from 17.4 percent in the previous quarter.

The average down payment for homes purchased by co-buyers nationwide was $63,117, 51 percent higher than the average down payment of $41,749 for homes purchased by other homebuyers. The average co-buyer down payment represented 16.3 percent, more than double the average down payment percentage of 8.1 percent for other homebuyers.

Among 153 metropolitan statistical areas analyzed for co-buyer share, those with the highest percentage of co-buyers in Q2 2018 were San Jose, California (49.3 percent); San Francisco, California (39.1 percent); Honolulu, Hawaii (31.8 percent); Seattle, Washington (29.5 percent); and Miami, Florida (29.1 percent).

FHA loan share decreases to more than 10-year low

Residential loans backed by the Federal Housing Administration (FHA) accounted for 10.2 percent of all residential property loans originated in Q2 2018, down from 10.9 percent in the previous quarter and down from 13.5 percent a year ago to the lowest share since Q1 2008 — a more than 10-year low.

Residential loans backed by the U.S. Department of Veterans Affairs (VA) accounted for 5.4 percent of all residential property loans originated in Q2 2018, down from 6.2 percent in the previous quarter and down from 6.4 percent a year ago.

Report methodology

ATTOM Data Solutions analyzed recorded mortgage and deed of trust data for single family homes, condos, town homes and multi-family properties of two to four units for this report. Each recorded mortgage or deed of trust was counted as a separate loan origination. Dollar volume was calculated by multiplying the total number of loan originations by the average loan amount for those loan originations. Origination counts and dollar volumes are projected for the most recent two quarters based on historical share of mortgage and deed of trust data recorded and collected within 45 days from the end of a quarter — which is when ATTOM pulls data for the report.

About ATTOM Data Solutions

ATTOM Data Solutions provides premium property data to power products that improve transparency, innovation, efficiency and disruption in a data-driven economy. ATTOM multi-sources property tax, deed, mortgage, foreclosure, environmental risk, natural hazard, and neighborhood data for more than 155 million U.S. residential and commercial properties covering 99 percent of the nation’s population. A rigorous data management process involving more than 20 steps validates, standardizes and enhances the data collected by ATTOM, assigning each property record with a persistent, unique ID — the ATTOM ID. The 9TB ATTOM Data Warehouse fuels innovation in many industries including mortgage, real estate, insurance, marketing, government and more through flexible data delivery solutions that include bulk file licenses, APIs, market trends, marketing lists, match & append and more.

Media Contact:

Christine Stricker

949.748.8428

christine.stricker@attomdata.com

Data and Report Licensing:

949.502.8313

datareports@attomdata.com