The following is an excerpt from a white paper published by ATTOM Data Solutions. The full 12-page white paper with exclusive data and charts from ATTOM, along with more insights from thought leaders in predictive analytics, is available for free download here.

Subprime financing is on the upswing, and for a lot of people that’s a problem. The mortgage meltdown is widely identified with subprime lending so why should the return of such loans be welcomed?

“Riskier U.S. mortgages are creeping back into the bond market again,” reported Bloomberg in May. “The loans in question are nowhere near the toxic mortgages that brought down the financial system last decade. But they’re being made to people with lower credit scores and with more debt relative to their income.”

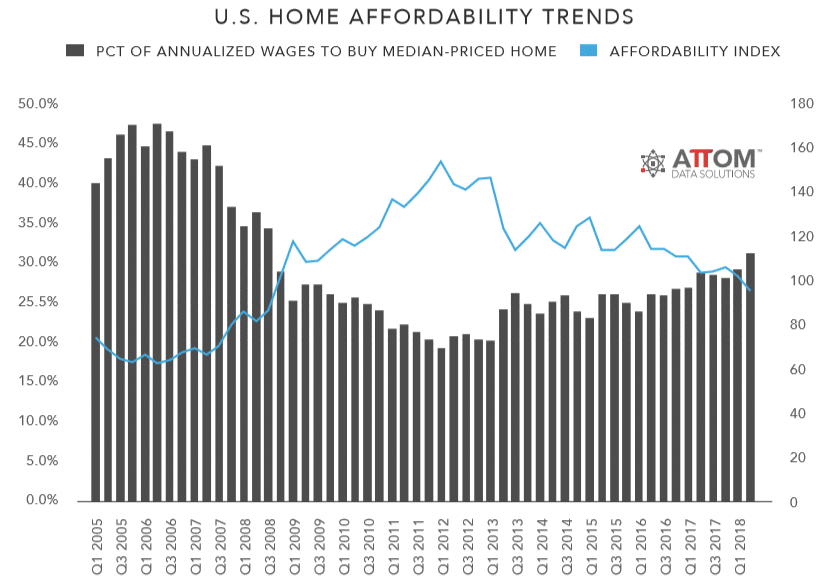

Average wage earners purchasing a home at the U.S. median sales price of $245,000 in Q2 2018 would need to spend 31.2 percent of their gross income on the monthly house payment for that home — assuming 3 percent down and including mortgage, property taxes, and insurance, according to the ATTOM Data Solutions Q2 2018 U.S. Home Affordability Report.

That 31.2 percent of average wages needed to purchase a median-priced home in the second quarter of 2018 is the highest in nearly 10 years. Back in 2008 the share of income needed to buy was 34.3 percent.

What was previously known as subprime is now increasingly branded as nonprime to differentiate it from past loan offerings. But whatever its called, why is subprime returning,? Isn’t the economy doing well with little unemployment and strong numbers on Wall Street? If subprime is back, will we see the return of the old shortcuts and abuses? Or something different?

the reality is that many potential borrowers can’t crack the mortgage application code. The Qualified Mortgage (QM) standards can be tough and inflexible, especially for borrowers with stalled incomes and mounting debts. There are few places for them to turn. As Mike Fratantoni, chief economist with the Mortgage Bankers Association, explains, 98 to 99 percent of all loans now originated are QMs.

It doesn’t have to be this way. Not only are there QM loans, lenders are also allowed to originate non-QM financing such as jumbo mortgages and nonprime financing. Nonprime loans provide a path to mortgage financing for borrowers hobbled with low credit scores, debt issues and other concerns, but whom some lenders consider to still be good mortgage risks.

The Nonprime Alternative

There’s no standard definition for such terms as subprime, nonprime or near-prime. It’s not just a credit score of 550, 600 or 620. The Consumer Financial Protection Bureau (CFPB) says that a subprime loan is “generally a loan that is meant to be offered to prospective borrowers with impaired credit records. The higher interest rate is intended to compensate the lender for accepting the greater risk in lending to such borrowers.”

In reality nonprime status can be triggered by a variety of factors. Borrowers may find they do not qualify for prime financing because their debt payments are too high (DTI issues), they lack reserves, the property does not provide enough security for the loan (LTV concerns), or their paperwork does not meet the usual standards — a particular problem for the self-employed and small business owners.

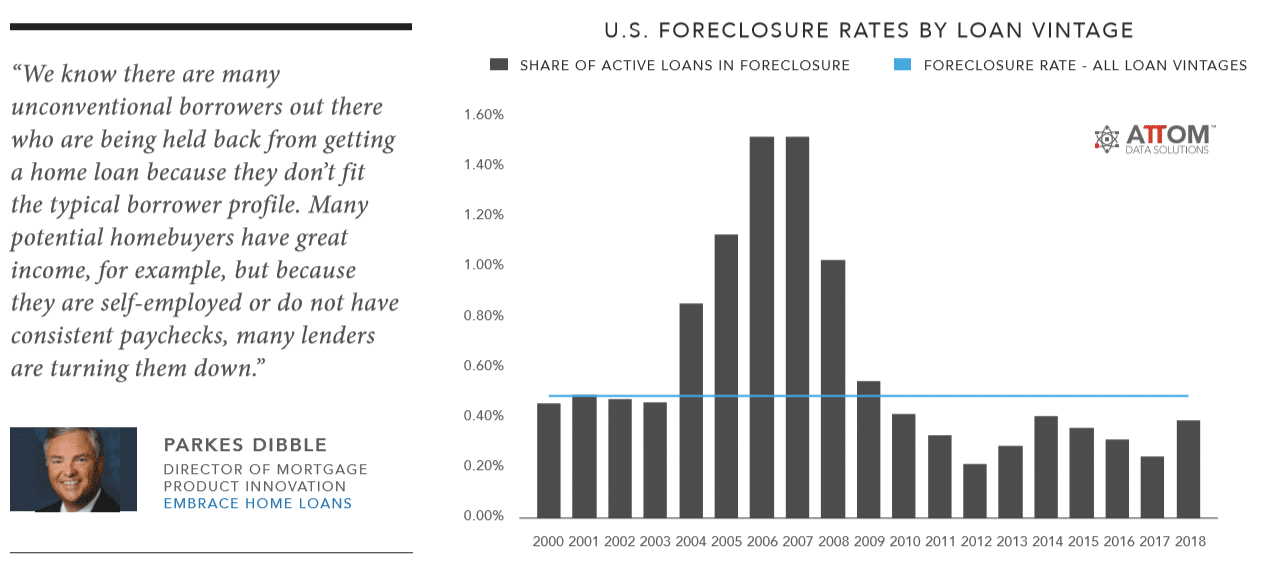

“We know there are many unconventional borrowers out there who are being held back from getting a home loan because they don’t fit the typical borrower profile,” said Parkes Dibble, director of mortgage product innovation with Embrace Home Loans. “Many potential homebuyers have great income, for example, but because they are self-employed or do not have consistent paychecks, many lenders are turning them down.”

Right now nonprime activity is just a small part of the overall mortgage marketplace, but that may be changing. Tom Schopflocher and Jeremy Schneider with S&P Global Ratings explained in a December report that “because not everyone is eligible for a QM loan, some would-be homeowners have been unable to get conventional financing because they can’t or don’t provide standard documentation (e.g., W-2s) or because they have recently experienced a credit event. The demand from those who fall outside the conventional credit box has created a niche market for lenders prepared to provide non-QM loans.”

While a lot of attention has been given to the use of automation and artificial intelligence for mortgage underwriting, that’s not the approach used in some nonprime programs.

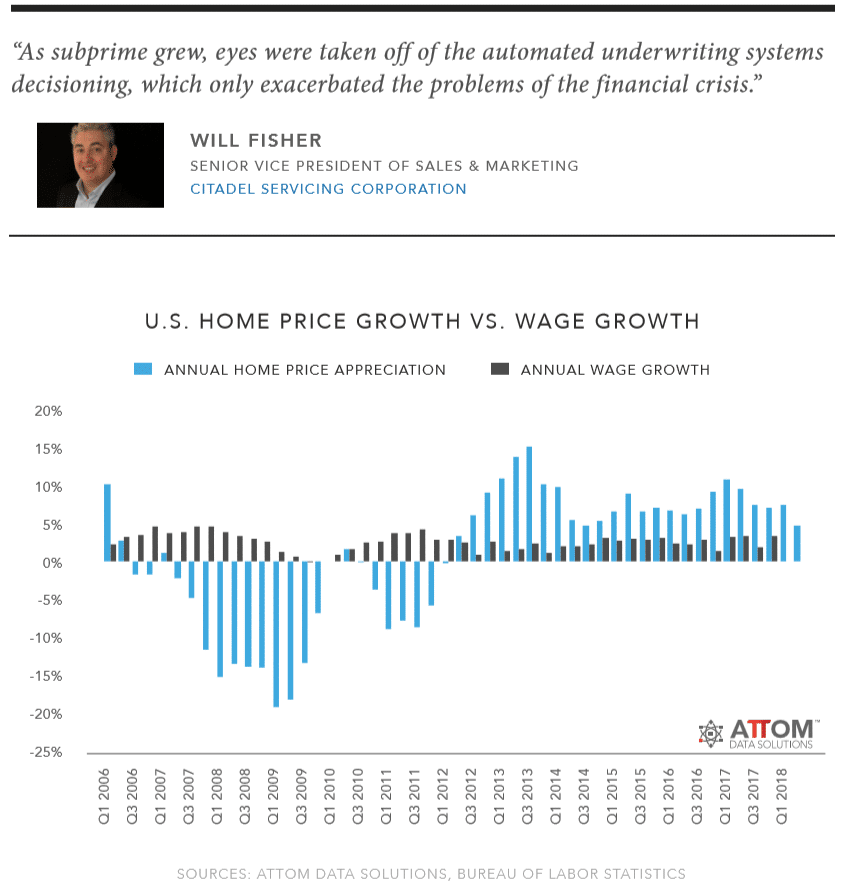

“At the present time we don’t view any AI programs robust enough to handle the intricacies of nonprime loans,” says Will Fisher, senior vice president of sales & marketing with Citadel Servicing Corporation. “Additionally, if you look at the past, lenders tried to automate subprime lending only to find that individuals were able to game the software and fund bad loans. As subprime grew, eyes were taken off of the automated underwriting systems decisioning, which only exacerbated the problems of the financial crisis.