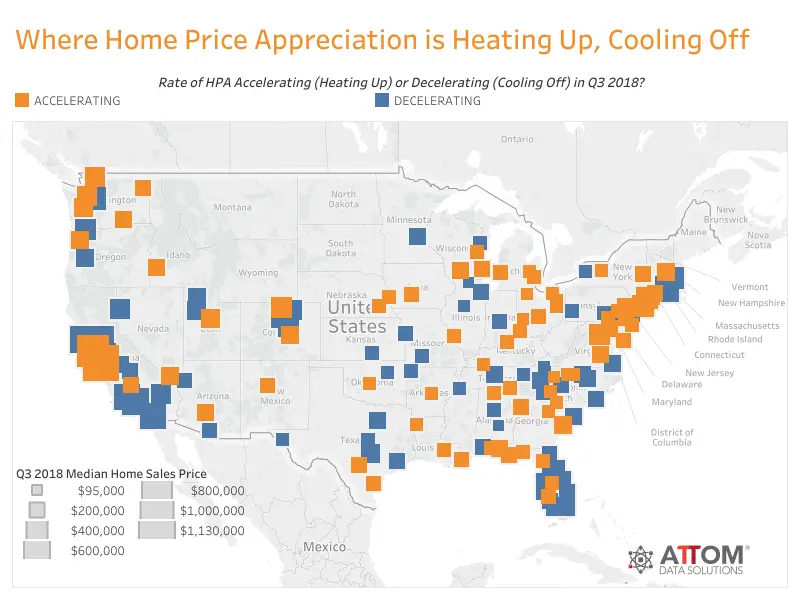

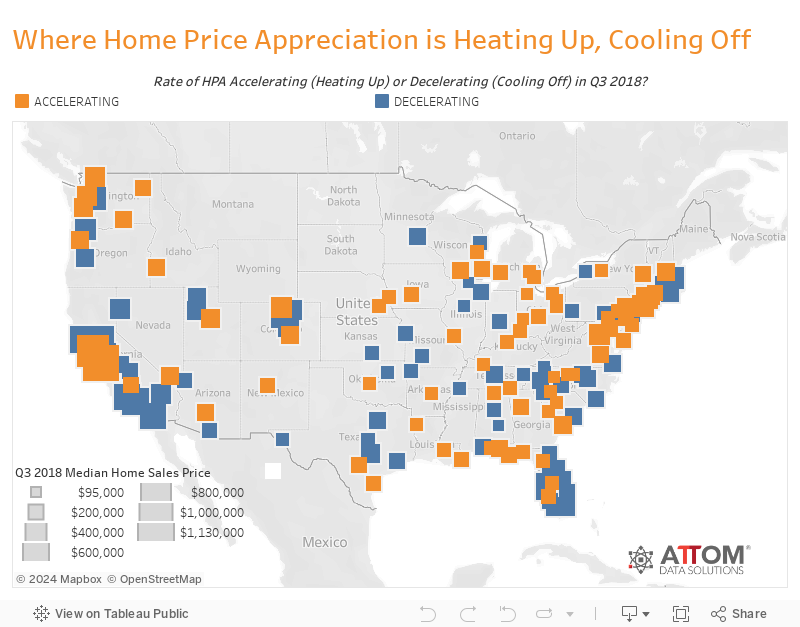

Annual Home Price Appreciation (HPA) Slows in 49 Percent of Local Markets;

San Jose, Boise, Las Vegas Among Markets Bucking National Trend with Accelerating HPA;

IRVINE, Calif. – Oct. 25, 2018 — ATTOM Data Solutions, curator of the nation’s premier property database, today released its Q3 2018 U.S. Home Sales Report, which shows that U.S. single family homes and condos sold for a median price of $256,000 in the third quarter, up 1.0 percent from the previous quarter and up 4.8 percent from a year ago — the slowest pace of annual home price appreciation since Q2 2016. For a detailed home sales data analysis, click here.

“The continued slowdown in the rate of home price appreciation nationwide and in many local markets is a rational response to worsening home affordability — which has deteriorated at an accelerated pace this year due to rising mortgage rates,” said Daren Blomquist, senior vice president at ATTOM Data Solutions. “Markets not experiencing this price appreciation cooldown may have more of an affordability cushion to work with, but some are in danger of overheating if home price gains continue to run hot.”

Rate of home price appreciation slows in Los Angeles, Chicago, Dallas-Fort Worth

The rate of home price appreciation slowed compared to a year ago in 74 of the 150 metropolitan statistical areas analyzed for median home prices (49 percent), including Los Angeles, Chicago, Dallas-Fort Worth, Houston and Miami — all of which posted single-digit percentage gains in median home prices compared to a year ago.

“I think the key factor underpinning the decelerating price appreciation is the impact of rising rates on the monthly payment,” said Tendayi Kapfidze, chief economist at mortgage marketplace LendingTree. “Absent financing structures that allow a borrower to increase leverage while mitigating an increase in the monthly debt service, buying power is decreasing across the board.

“This especially affects the marginal buyer who doesn’t have a lot of wiggle room,” Kapfidze added. “And if you remember your econ 101, the marginal buyer transacts at the market clearing price. So while there is still strong demand, some potential buyers are falling out of the market and others are moving down in price with the aggregate effect being a moderation in price appreciation.”

Rate of home price appreciation continues to accelerate in San Jose, Boise, Las Vegas

Counter to the national trend, the rate of home price appreciation accelerated in 76 of the 150 metro areas analyzed in the report (51 percent), including San Jose, California; Boise, Idaho; Las Vegas, Nevada; Grand Rapids, Michigan; Lakeland, Florida; Colorado Springs, Colorado; Dayton, Ohio; San Francisco, California; and Atlanta, Georgia — all of which posted double-digit percentage gains in median home prices compared to a year ago.

“Housing affordability is becoming an increasingly big issue, especially in the western U.S. where many markets have not seen adequate new construction — putting substantial upward pricing pressure on resale homes,” said Matthew Gardner, chief economist with Seattle-based Windermere Real Estate, noting that the rate of home price appreciation in the Seattle metro area slowed to the slowest pace since Q4 2014. “Seattle is one of these areas, and home price growth is likely to continue to slow there until incomes are able to catch up — even given significant demand from robust employment growth.

“On the other hand, markets such as Boise, Idaho, are building at a brisk pace, and that is allowing ongoing resale price appreciation as new supply keeps the market relatively affordable,” Gardner added.

Median home prices above pre-recession levels in 69 percent of markets

Median home prices nationwide in Q3 2018 were 11 percent above the pre-recession peak of $230,000 in Q3 2005 and 77 percent above the post-recession trough of $145,000 in Q1 2012.

Median home prices in Q3 2018 were above their pre-recession peak in 103 of the 150 metro areas analyzed for median prices (69 percent), led by Dallas-Fort Worth, Texas (86 percent above); Houston, Texas (85 percent above); Kennewick-Richland, Washington (81 percent above); Greeley, Colorado (77 percent above); and San Antonio (73 percent above).

Median home prices in Q3 2018 were below their pre-recession peak in 47 of the 150 metro areas analyzed for median prices (31 percent), led by Montgomery, Alabama (32 percent below); York, Pennsylvania (32 percent below); Atlantic City, New Jersey (30 percent below); Naples, Florida (20 percent below); and Cape Coral-Fort Myers, Florida (16 percent below).

Average homeownership tenure increases to new all-time high of 8.23 years

U.S. homeowners who sold in Q3 2018 had owned their homes an average of 8.23 years, up from an average homeownership tenure of 7.97 years in Q2 2018 and up from 7.98 years in Q3 2017 to a new record high going back as far as homeownership tenure data is available, Q1 2000.

Among 108 metropolitan statistical areas analyzed for homeownership tenure, those with the shortest average homeownership tenure were Oklahoma City, Oklahoma (6.31 years), Denver, Colorado (7.17 years); Colorado Springs, Colorado (7.18 years); Austin, Texas (7.24 years); and Provo-Orem, Utah (7.24 years).

Counter to the national trend, 19 of the 108 metropolitan statistical areas analyzed for homeownership tenure posted a year-over-year decrease in average homeownership tenure, including Boston, Phoenix, Seattle, Denver and Nashville.

Q3 2018 home sellers gained average of $61,232 since purchase

Homeowners who sold in Q3 2018 sold for an average of $61,232 more than their original purchase price, the highest average home seller price gain since Q2 2007. The $61,232 average home seller price gain in Q3 2018 represented an average 32.3 percent return on the original purchase price, up from an average 31.6 percent return in the previous quarter and up from an average 31.4 percent return in Q3 2017 — although still below recent peak of 32.5 percent in Q4 2017.

Among 156 metropolitan statistical areas analyzed for average home seller gains, those with the highest average home seller percentage gains were San Jose, California (108.7 percent gain); San Francisco, California (77.3 percent gain); Seattle, Washington (69.8 percent gain); Santa Rosa, California (67.9 percent gain); and Salem, Oregon (63.4 percent gain).

Along with San Jose, San Francisco and Seattle, other metro areas with a population of at least 1 million and average home seller percentage gains of more than 55 percent were Portland, Oregon (59.6 percent gain); Boston Massachusetts (58.1 percent gain); Los Angeles, California (58.0 percent gain); Nashville, Tennessee (56.5 percent gain); and Salt Lake City, Utah (56.5 percent).

Distressed sales rebound from 11-year low in previous quarter

Distressed sales — sales of bank-owned homes, short sales, and sales to third-party investors at foreclosure auction — accounted for 11.6 percent of all U.S. single family home and condo sales in Q3 2018, up from an 11-year low of 11.2 percent in the previous quarter but still down from 12.8 percent in Q3 2017.

Counter to the national trend, 32 of 152 metropolitan statistical areas analyzed for distressed sales (21 percent) posted a year-over-year increase in share of distressed sales, including Houston (up 5 percent), Denver (up 6 percent); San Antonio (up 5 percent); Kansas City (up 9 percent); and Milwaukee (up 6 percent).

Metros with the highest share of distressed sales in Q3 2018 were Montgomery, Alabama (32.7 percent of sales); Atlantic City, New Jersey (32.2 percent); Youngstown, Ohio (23.2 percent); Columbus, Georgia (22.2 percent); and McAllen, Texas (21.9 percent).

Other report findings

- All-cash purchases accounted for 27.0 percent of all single family home and condo sales in Q3 2018, down from 27.4 percent in the previous quarter but still up from 26.5 percent in Q3 2017.

- Sales to institutional investors (entities buying at least 10 properties in a calendar year) accounted for 2.8 percent of all single family home and condo sales in Q3 2018, up from 2.1 percent in the previous quarter but still down from 3.0 percent in Q3 2017.

- Sales to buyers using FHA loans — typically first-time homebuyers — accounted for 10.3 percent of all sales of single family homes and condos in Q3 2018, up from 9.9 percent in the previous quarter but still down from 13.3 percent in Q3 2017.

###

Report methodology

Data for the ATTOM Data Solutions U.S. Home Sales Report is derived from recorded sales deeds, foreclosure filings and loan data. Statistics for previous quarters are revised when each new report is issued as more deed data becomes available for those previous months. Median sales prices are calculated based on the sales price on the publicly recorded sales deed when available. If no sales price is recorded then the purchase loan amount is used to calculate median price, and if no purchase loan amount is available, the property’s Automated Valuation Model (AVM) at time of sale is used to calculate the median price.

Definitions

All-cash purchases: sales where no loan is recorded at the time of sale and where ATTOM has coverage of loan data.

Institutional investor purchases: residential property sales to non-lending entities that purchased at least 10 properties in a calendar year.

REO sale: a sale of a property that occurs while the property is actively bank owned (REO).

Third-party foreclosure auction sale: a sale of a property that occurs at the public foreclosure auction (trustee’s sale or sheriff’s sale) in which the property is sold to a third-party buyer and does not transfer back to the foreclosing bank.

Short sale: a sale of a property where the sale price is less than (short) the combined amount of loans secured by the property.

About ATTOM Data Solutions

ATTOM Data Solutions provides premium property data to power products that improve transparency, innovation, efficiency and disruption in a data-driven economy. ATTOM multi-sources property tax, deed, mortgage, foreclosure, environmental risk, natural hazard, and neighborhood data for more than 155 million U.S. residential and commercial properties covering 99 percent of the nation’s population. A rigorous data management process involving more than 20 steps validates, standardizes and enhances the data collected by ATTOM, assigning each property record with a persistent, unique ID — the ATTOM ID. The 9TB ATTOM Data Warehouse fuels innovation in many industries including mortgage, real estate, insurance, marketing, government and more through flexible data delivery solutions that include bulk file licenses, APIs, market trends, marketing lists, match & append and more.

Media Contact:

Christine Stricker

949.748.8428

christine.stricker@attomdata.com

Data and Report Licensing:

949.502.8313

datareports@attomdata.com