Returns Drop for First Time in Over Two Years and Decline at Fastest Pace in 10 Years; Median U.S. Home Price Up Just 2 Percent Quarterly, to New High of $320,500

IRVINE, Calif. – Apr. 28, 2022 — ATTOM, a leading curator of real estate data nationwide for land and property data, today released its first-quarter 2022 U.S. Home Sales Report, which shows that profit margins on median-priced single-family home sales across the United States dipped to 47.2 percent – the first quarterly decline since late 2019 and the largest in a decade.

In a sign that the nationwide housing-market boom may be slowing, the latest profit margin was down from 51.6 percent in the fourth quarter of 2021. While profit margins often decrease during the relatively slow Winter home-buying season, the latest dip of more than four percentage points marked the first quarterly decline since the fourth quarter of 2019 and the largest since the first quarter of 2011.

The report reveals that the typical return on investment remained historically high, easily topping the 37.5 percent level recorded in the first quarter of 2021 and almost 20 points above the 29.4 percent figure from the first quarter of 2019.

Gross profits, while also near record highs, followed a similar pattern in the first quarter of 2022. The typical single-family home sale across the country generated a gross first-quarter profit of $103,000, down from $107,187 in the fourth quarter of last year, although still well above $75,001 a year earlier.

“Home prices simply can’t continue to go up as rapidly as they have for the past few years,” said Rick Sharga, executive vice president of market intelligence for ATTOM. “The combination of higher prices, rising mortgage rates, and the highest rates of inflation in 40 years may be pricing some prospective buyers out of the market, which means we may begin to see lower sales numbers. Ultimately, as affordability worsens, price appreciation should slow down, and we may even see modest price corrections in some markets.”

The lower gross profits came as the national median home price increased just 1.7 percent, from $315,000 in the fourth quarter of 2021 to $320,500 in the first quarter of this year. That marked the ninth straight quarterly record and was up 16.5 percent from the first quarter of 2021. But the modest quarterly gain fell below price spikes that first-quarter sellers commonly were paying when they originally bought their homes, which led to the decline in profits.

Home sales also lagged behind the numbers from the first quarter of 2021, with sales falling from 1.2 million to 1.1 million. These sales, pricing. and profit trends point to the possibility of a calmer period in a housing market that has largely roared ahead over the past two years, both in spite of and because of the ongoing economic threat posed by Coronavirus pandemic that hit early in 2020.

A surge of buyers largely unscathed financially by the pandemic has flooded the market over that period, chasing a historically limited supply of homes for sale and driving up prices. That happened amid a period of rock-bottom mortgage rates that dipped below 3 percent for a 30-year fixed-rate loan, and a desire of many households to trade congested virus-prone parts of the country for the relative safety of a house and yard along with larger spaces for developing work-at-home lifestyles.

But even as employment has grown over the past year, interest rates are rising, which has cut into what buyers can afford. The nation’s inflation rate, meanwhile, is at a 40-year high, generating further economic uncertainty that could stifle home-price increases.

Profit margins decline quarterly in over 40 percent of metro areas around the U.S.

Typical profit margins – the percent change between median purchase and resale prices – fell from the fourth quarter of 2021 to the first quarter of 2022 in 71 (42 percent) of the 170 metro areas around the U.S. with sufficient data to analyze. That trend emerged even as investment returns remained up annually in 152 (89 percent) of those metros. Metro areas were included if they had at least 1,000 single-family home sales in the first quarter of 2022 and a population of at least 200,000.

The biggest quarterly decreases in profit margins came in the metro areas of Santa Barbara, CA (margin down from 72.9 percent in the fourth quarter of 2021 to 45.8 percent in the first quarter of 2022); Boise, ID (down from 110.4 percent to 88.8 percent); Brownsville, TX (down from 54.3 percent to 38.1 percent); St. Louis, MO (down from 37.6 percent to 23.9 percent) and Des Moines, IA (down from 48.1 percent to 35.2 percent).

Aside from St. Louis, the biggest quarterly profit-margin decreases in metro areas with a population of at least 1 million in the first quarter of 2022 were in Raleigh, NC (margin down from 53.1 percent to 40.7 percent); Sacramento, CA (down from 63.9 percent to 52.1 percent); Minneapolis, MN (down from 40 percent to 32 percent) and Atlanta, GA (down from 38.5 percent to 31 percent).

Profit margins increased quarterly in 99 of the 170 metro areas analyzed (58 percent). The biggest quarterly increases were in Kingsport, TN (margin up from 51.1 percent in the fourth quarter of 2021 to 71.1 percent in the first quarter of 2022); Rochester, NY (up from 57.1 percent to 76.3 percent); Lake Havasu City, AZ (up from 58.2 percent to 75.2 percent); Cape Coral-Fort Myers, FL (up from 64.2 percent to 80.9 percent) and Toledo, OH (up from 39.8 percent to 53.3 percent).

Aside from Rochester, the largest quarterly increases in profit margins among metro areas with a population of at least 1 million came in Honolulu, HI (up from 34.8 percent to 47.6 percent); Richmond, VA (up from 48.2 percent to 60 percent); Oklahoma City, OK (up from 30 percent to 38.6 percent) and New Orleans, LA (up from 27.6 to 34.4 percent).

Largest profit margins again in West; smallest in South and Midwest

The West continued to have the largest profit margins on typical single-family home sales around the country, with 13 of the top 25 returns on investment in the first quarter of 2022 from among the 170 metropolitan areas with enough data to analyze. The highest profit margins were in Hilo, HI (96.4 percent return); Scranton, PA (91.2 percent); Boise, ID (88.8 percent); San Jose, CA (86.1 percent) and Spokane, WA (85 percent).

Twenty-one of the 25 smallest margins were in the South and Midwest regions of the country. The lowest were in Lafayette, LA (16.6 percent); Shreveport, LA (17.1 percent); Columbus, GA (19.2 percent); Little Rock, AR (21.3 percent) and Lakeland, FL (22.9 percent).

Prices up quarterly in just half the nation

Median home prices in the first quarter of 2022 exceeded values from the prior quarter in only 89 (52 percent) of the 170 metropolitan statistical areas with enough data to analyze, even though they remained up annually in 165 of those metros (97 percent). Nationally, the median price of $320,500 in the first quarter was up from $315,000 in the fourth quarter of 2021 and $275,000 in the first quarter of last year.

The biggest quarterly increases in median home prices during the first quarter of 2022 were in Honolulu, HI (up 7.9 percent); Port St. Lucie, FL (up 7.7 percent); Lakeland, FL (up 7.6 percent); Austin, TX (up 7.6 percent) and Cape Coral-Fort Myers, FL (up 7.5 percent).

Aside from Honolulu and Austin, the largest quarterly increases in metro areas with a population of at least 1 million in the first quarter of 2022 were in Atlanta, GA (up 6.5 percent); Las Vegas, NV (up 6.4 percent) and San Diego, CA (up 6.4 percent).

Home prices in the first quarter of 2022 hit or tied all-time highs in 47 percent of the metro areas in the report, including New York, NY; Los Angeles, CA; Dallas, TX; Houston, TX, and Miami, FL.

The largest quarterly decreases in median prices during the first quarter of 2022 were in Macon, GA (down 15.4 percent); Kalamazoo, MI (down 10.9 percent); Detroit, MI (down 10 percent); York, PA (down 9.5 percent) and Des Moines, IA (down 9.3 percent).

Aside from Detroit, the largest quarterly decreases in metro areas with a population of at least 1 million in the first quarter of 2022 were in Rochester, NY (down 9.1 percent); Buffalo, NY (down 7.5 percent); Indianapolis, IN (down 6.6 percent) and Pittsburgh, PA (down 6.1 percent).

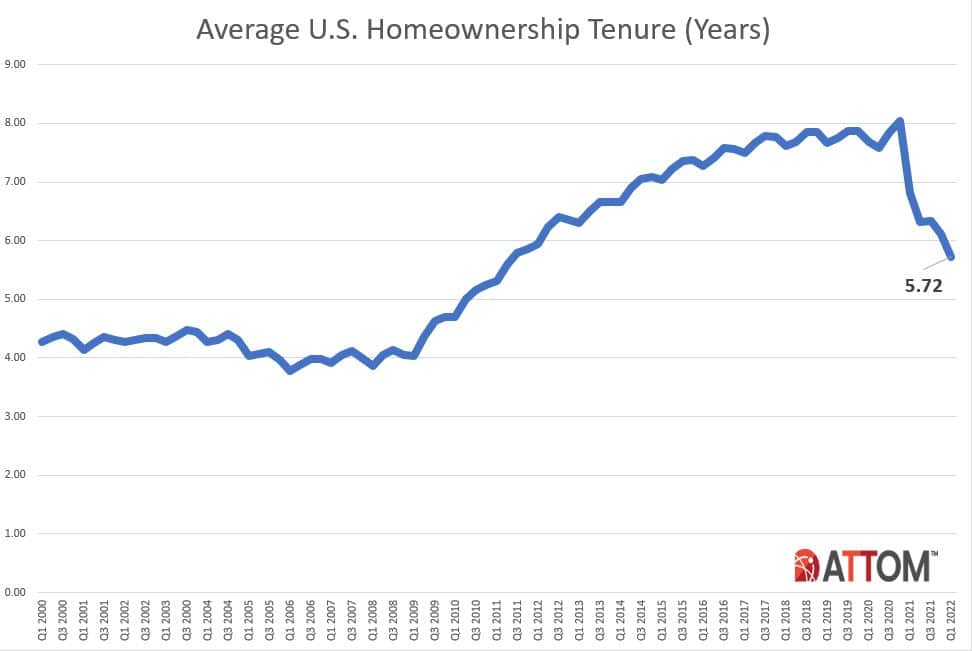

Homeownership tenure drops again, to 11-year low

Homeowners who sold in the first quarter of 2022 had owned their homes an average of 5.72 years, down from 6.12 years in the fourth quarter of 2021 and down by more than a year from 6.82 years in the first quarter of 2021. The latest figure marked the shortest average time between purchase and resale since the second quarter of 2011.

Tenure decreased from the first quarter of 2021 to the same period this year in 94 percent of metro areas with sufficient data. They were led by Lakeland, FL (tenure down 82 percent); Salem, OR (down 55 percent); Cleveland, OH (down 47 percent); Las Vegas, NV (down 45 percent) and Provo, UT (down 40 percent).

“Existing home sales typically account for 80-90 percent of all home sales, and increased homeownership tenure over the past decade has had an impact on the inventory of homes available for sale,” Sharga noted. “If we continue to see a reversal of that trend, it could bring desperately needed supply back to the market, which would help stabilize prices.”

Eight of the 10 longest average tenures among sellers in the first quarter of 2022 were in the Northeast or West regions. They were led by Honolulu, HI (8.54 years); Bellingham, WA (8.31 years); Manchester, NH (7.79 years); Hilo, HI (7.65 years) and New Haven, CT (7.6 years).

The smallest average tenures among first-quarter sellers were in Lakeland, FL (1.28 years); Memphis, TN (3.45 years); Tucson, AZ (3.59 years); Cleveland, OH (4.08 years) and Provo, UT (4.24 years).

Lender-owned foreclosure sales remain at lowest point this century

Home sales following foreclosures by banks and other lenders represented just 1.2 percent of all U.S. single-family home sales in the first quarter of 2022. That was at or below the smallest portion since at least the first quarter of 2000.

The latest portion of REO sales matched the 1.2 percent figure from the fourth quarter of 2021 and was down from 2.1 percent in the first quarter of last year. REO sales represented only one of every 87 sales in the first quarter of 2022 compared to the peak this century of one in three in first quarter of 2009.

Among metropolitan statistical areas with a population of at least 200,000 and sufficient data, those areas where so-called REO sales represented the largest portion of all sales in the first quarter of 2022 included Davenport, IA (4.9 percent); St. Louis, MO (4.2 percent); Flint, MI (3.3 percent); Hartford, CT (3.1 percent) and New Haven, CT (3.1 percent).

Cash sales at seven-year high

Nationwide, all-cash purchases accounted for 34.2 percent of all single-family home sales in the first quarter of 2022, the highest level since the first quarter of 2015. The first-quarter 2022 number was up from 32 percent in the fourth quarter of 2021 and from 30.3 percent in the first quarter of last year.

Among metropolitan statistical areas with a population of at least 200,000 and sufficient cash-sales data, those where cash sales represented the largest share all transactions in the first quarter of 2022 included Flint, MI (61.8 percent of all sales); Detroit, MI (61.5 percent); Utica, NY (54.8 percent); Naples, FL (54.4 percent) and Ann Arbor, MI (53 percent).

Those where cash sales represented the smallest share of all transactions in the first quarter of 2022 included Kennewick, WA (17.2 percent of all sales); Augusta, GA (17.9 percent); Lincoln, NE (18.1 percent); Washington, DC (19.4 percent) and San Jose, CA (19.4 percent).

Institutional investment down by more than half

Institutional investors nationwide accounted for just 4.1 percent, or one of every 24 all single-family home purchases in the first quarter of 2022 – less than half the 9.1 percent level in the fourth quarter of 2021. The latest figure also was down from 5.4 percent in the first quarter of 2021.

“For those people who still believe the theory that institutional investors are buying up all the available inventory, the numbers in our Q1 2022 report offer a pretty strong rebuttal,” Sharga added. “It’s also interesting that cash sales – often attributed to institutional investors – continued to increase even as investor activity diminished.”

Among states with enough data to analyze, those with the largest percentages of sales to institutional investors in the first quarter of 2022 were Arizona (10.7 percent of all sales), Georgia (9.3 percent), North Carolina (8.7 percent), Nevada (8.4 percent) and Texas (6.1 percent).

States with the smallest levels of sales to institutional investors in the first quarter of 2022 included Louisiana (0.5 percent), Connecticut (0.5 percent), Hawaii (0.6 percent), New York (0.7 percent) and Massachusetts (0.7 percent).

FHA-financed purchases at lowest level in more than 14 years

Nationwide, buyers using Federal Housing Administration (FHA) loans comprised only 7.3 percent of all single-family home purchases in the first quarter of 2022 (one of every 14), the lowest portion since the first quarter of 2008. The latest figure was down from 8.2 percent in the previous quarter and from 9.2 percent a year earlier.

Among metropolitan statistical areas with a population of at least 200,000 and sufficient FHA-buyer data, those with the highest levels of FHA buyers in the first quarter of 2022 included Visalia. CA (17.7 percent); Bakersfield, CA (16.7 percent); Shreveport, LA (16.3 percent); Mobile, AL (15.9 percent) and Yuma, A (15.7 percent).

###

Report methodology

The ATTOM U.S. Home Sales Report provides percentages of REO sales and all sales that are sold to institutional investors and cash buyers, at the state and metropolitan statistical area. Data is also available at the county and zip code level upon request. The data is derived from recorded sales deeds, foreclosure filings and loan data. Statistics for previous quarters are revised when each new report is issued as more deed data becomes available.

Definitions

All-cash purchase: sale where no loan is recorded at the time of sale and where ATTOM has coverage of loan data.

Homeownership tenure: for a given market and given quarter, the average time between the most recent sale date and the previous sale date, expressed in years.

Home seller price gains: the difference between the median sales price of homes in a given market in a given quarter and the median sales price of the previous sale of those same homes, expressed both in a dollar amount and as a percentage of the previous median sales price.

Institutional investor purchases: residential property sales to non-lending entities that purchased at least 10 properties in a calendar year.

REO sale: a sale of a property that occurs while the property is actively bank owned (REO).

About ATTOM

ATTOM delivers AI-driven property intelligence built on one of the nation's most trusted property data assets, covering 160 million U.S. properties—99% of the population. Our engineered, multi-sourced real estate data spans property tax, deeds, mortgages, foreclosure, environmental risk, property conditions, natural hazards, neighborhood insights, and geospatial boundaries, rigorously validated for advanced analytics. ATTOM supports analytics and AI-driven applications through flexible delivery options including APIs, bulk licensing, cloud delivery, and the MCP Server for AI-powered, agentic access to engineered property data—enabling organizations to automate analysis and scale property intelligence across industries.

Media Contact:

Christine Stricker

949.748.8428

christine.stricker@attomdata.com

Data and Report Licensing:

949.502.8313