Typical home generated a 44.1 percent return on investment in first quarter; National median sales price stayed level quarter-over-quarter at $360,000

IRVINE, Calif. – April, 23, 2026 – ATTOM, the leading provider of property data, AI-powered analytics, and real estate intelligence solutions, today released its latest U.S. Home Sales Report, which shows that homeowners made a 44.1 percent profit on typical single-family home and condo sales during the first quarter of 2026. That was down from 47.2 percent in the previous quarter and from 50.2 percent in the first quarter of 2025.

That 44.1 percent profit margin is the lowest since the first quarter of 2021, continuing a gradual decline from the recent peak of 63.5 percent in the second quarter of 2022. Despite the drop, margins remain historically high compared to pre-pandemic levels.

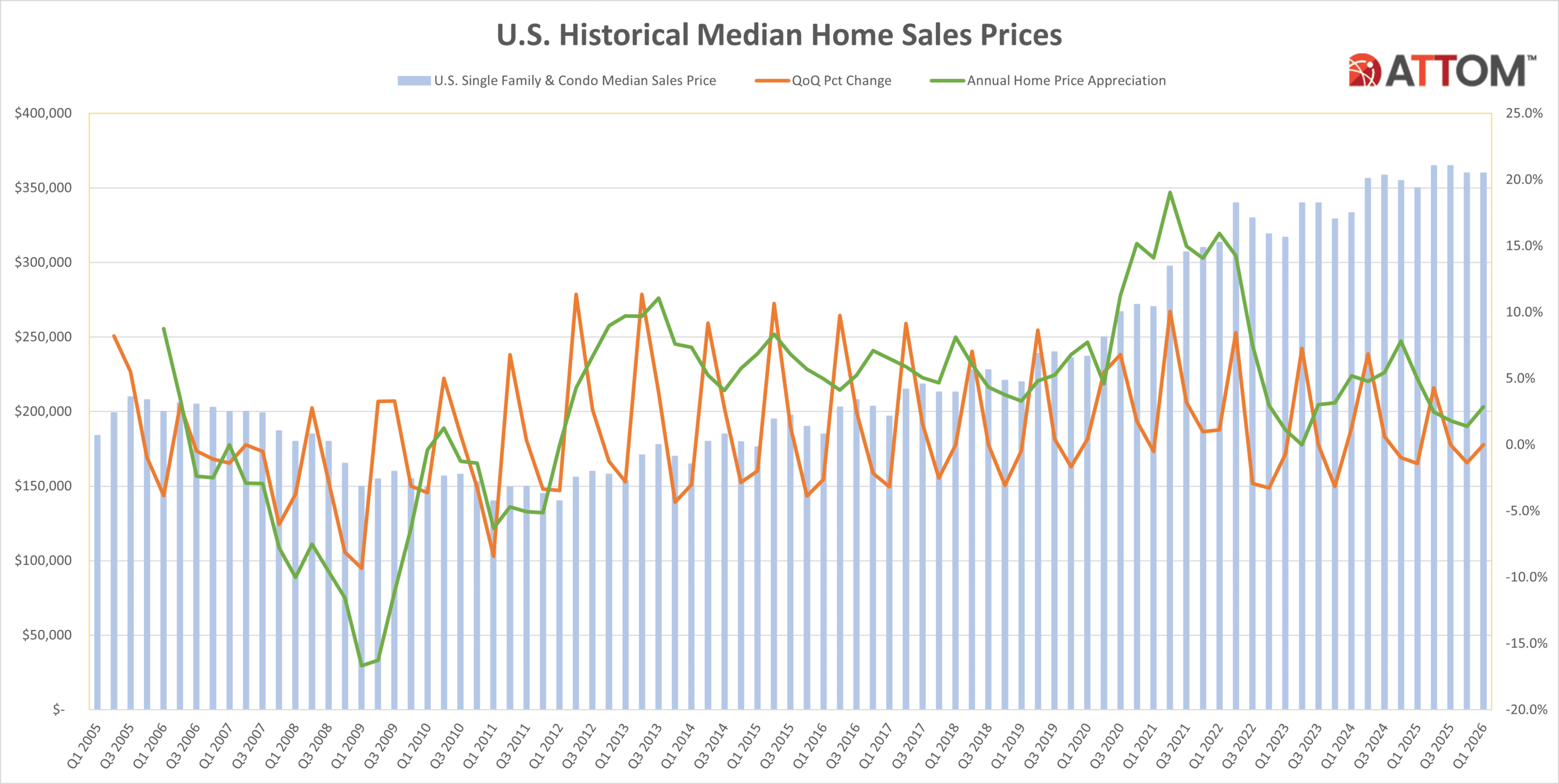

Home prices held steady quarter-over-quarter at $360,000 but were up 3 percent year-over-year from $350,000 in the first quarter of 2025.

Nationwide, the typical single-family home or condo sold for a raw profit of $110,100 in the first quarter of 2025, down 5 percent from the previous quarter and 6 percent from the same time last year.

“The first quarter is typically a slower sales season and that was compounded this year by rising mortgage rates,” said Rob Barber, CEO of ATTOM. “After the record high home prices we saw last summer, prices appear to be leveling out.”

“The profit margins sellers enjoyed over the last few years, which were consistently over 50 percent, were unusual,” he added. “But even with the most recent dip, margins are still well above the 30 percent return on investment sellers were seeing before the pandemic.”

Profit margins drop in Florida metros, rise in several Midwest metros

Seller profit margins fell quarter-over-quarter in 74.2 percent (95) of the 128 metropolitan statistical areas in ATTOM’s analysis. Metro areas were included in the report if they had more than 1,000 home sales in the first quarter of 2026 and sufficient data to analyze. Profit margins fell year-over-year in 82.8 percent (106) of the metros.

The metro areas with the largest annual falloffs in home sale profit margins were Ocala, FL (down from 119.4 percent in the first quarter of 2025 to 58.1 percent in the first quarter of 2026); Punta Gorda, FL (down from 78.9 percent to 54.3 percent); Lakeland, FL (down from 62.2 percent to 38 percent); North Port-Sarasota, FL (down from 57.9 percent to 35.5 percent); and Prescott, AZ (down from 69.4 percent to 47.1 percent).

The metros that saw the largest annual increases in profit margins were Flint, MI (up from 65.5 percent to 81.8 percent); Evansville, IN (up from 40.9 percent to 53.5 percent); Lansing, MI (up from 48 percent to 57.8 percent); Canton, OH (up from 55.5 percent to 60.2 percent); and Syracuse, NY (up from 67.6 percent to 72 percent).

Among metro areas with populations of at least 1 million, the largest annual drop-offs in profit margins were in Raleigh, NC (down from 49.8 percent to 33.1 percent); San Jose, CA (down from 88.5 percent to 74.8 percent); San Diego, CA (down from 69.4 percent to 56.6 percent); Sacramento, CA (down from 57.5 percent to 45.1 percent); and Buffalo, NY (down from 82.5 percent to 70.3 percent).

Margins remain low in major Texas cities

Of the 128 metros in ATTOM’s analysis, 37.5 percent (48) had typical home sale profit margins exceeding 50 percent in the first quarter.

Among metros with populations of at least 1 million, the largest typical profit margins were in San Jose, CA (74.8 percent); Hartford, CT (72.4 percent); Providence, RI (71.9 percent); Rochester, NY (70.5 percent); and Buffalo, NY (70.3 percent).

The lowest profit margins among those largest metros were in New Orleans, LA (14 percent); San Antonio, TX (19.9 percent); Houston, TX (25.4 percent); Dallas, TX (27.4 percent); and Austin, TX (27.4 percent).

Western cities boast highest profits in raw dollars

Nationwide, the typical home sale in the first quarter of 2026 generated $110,100 in raw profit.

Among metro areas with populations of at least 1 million, the largest year-over-year growth in raw profits were Birmingham, AL (up 16.9 percent); Honolulu, HI (up 13.9 percent); Detroit, MI (up 13.3 percent); Hartford, CT (up 7.1 percent); and Philadelphia, PA (up 6.8 percent).

The metros with populations of at least 1 million with the largest typical raw profits in the first quarter of 2026 were San Jose, CA ($652,500); San Francisco, CA ($375,00); Los Angeles, CA ($332,875); San Diego, CA ($320,000); and Seattle, WA ($284,450).

Of all metros analyzed, the smallest typical raw profits were in Beaumont, TX ($23,578); New Orleans, LA ($30,000); Killeen, TX ($33,415); Davenport, IA ($42,000); and Baton Rouge, LA ($44,000)

Median home prices rose in more than two thirds of metros

The national median home sales price held steady between the fourth quarter of 2025 and the first quarter of 2026 at $360,000, but the median sales prices rose annually in 68.2 percent (88) of the 129 metropolitan statistical areas with sufficient data to analyze.

The metro areas with the largest year-over-year increases in median sales prices were Birmingham, AL (up 17.5 percent); Detroit, MI (up 17.2 percent); Augusta, GA (up 12.5 percent); Syracuse, NY (up 11.8 percent); and Madison, WI (up 11.8 percent).

The metros with the largest year-over-year drops in median sales prices were Cape Coral, FL (down 9 percent); Durham, NC (down 8.7 percent); Austin, TX (down 7.2 percent); San Francisco, CA (down 7.2 percent); and Ocala, FL (down 7.2 percent).

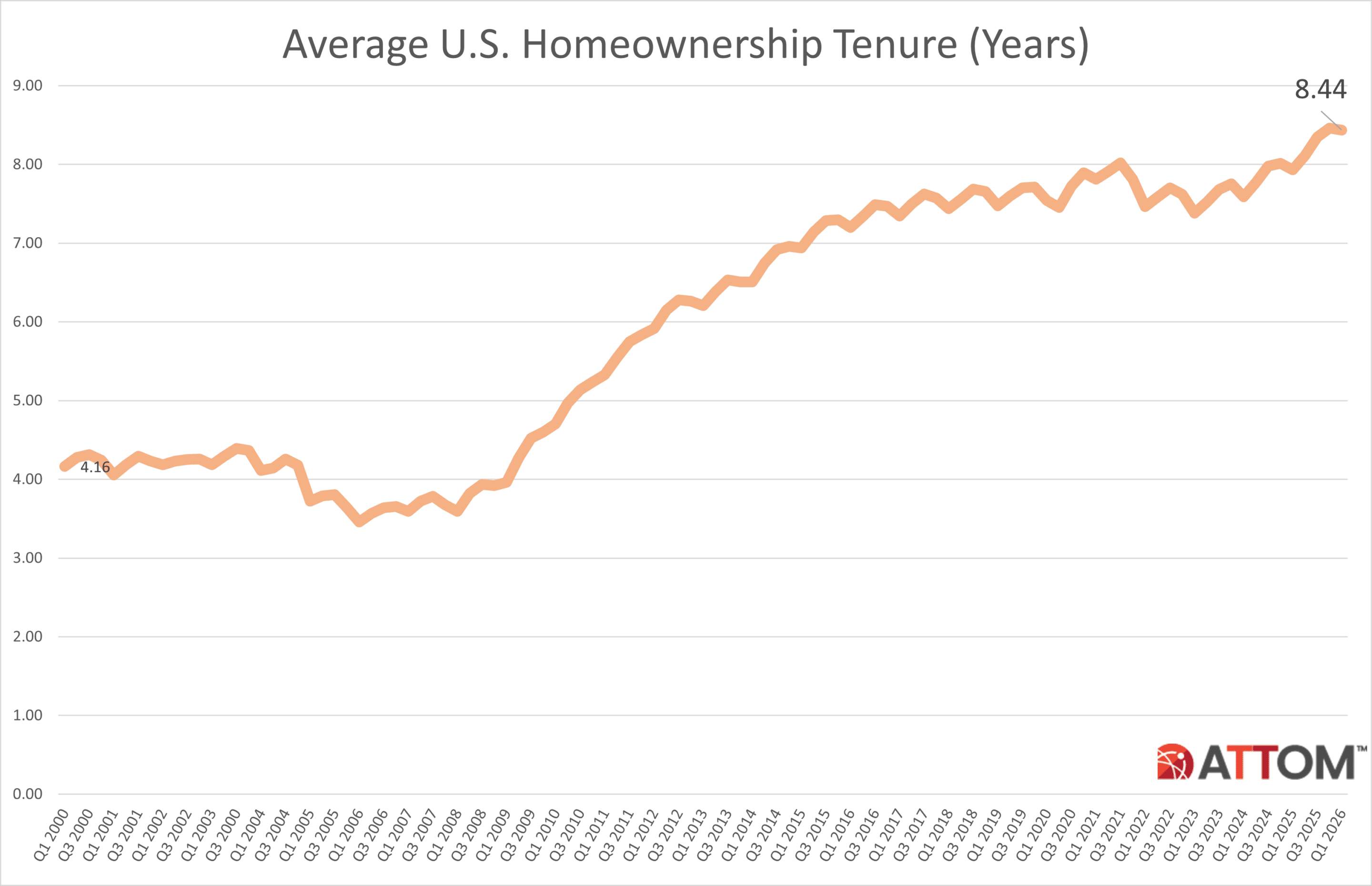

Homeownership tenure drops slightly nationwide

Owners who sold their homes in the first quarter of 2026 had held them for an average of 8.44 years, down slightly from the 8.46-year tenure for homes sold in the fourth quarter of 2025.

The metros with the longest average homeownership tenure—the time between purchase and sale—for homes sold in the first quarter of 2026 were Barnstable, MA (14.97 years); Napa, CA (12.65 years); Springfield, MA (12.64 years); Santa Rosa, CA (12.56 years); and San Francisco, CA (12.41 years).

The metros with the shortest homeownership tenures for homes sold in the first quarter of 2026 were Kansas City, MO (6.9 years); Provo, UT (7.07 years); San Antonio, TX (7.17 years); Oklahoma City, OK (7.24 years); and Panama City, FL (7.25 years).

Share of homes sold by lenders grows

In the first quarter of 2026, homes sold by banks or other lenders account for 1.6 percent of all home sales nationwide, up from 1.3 percent the previous quarter and 1.5 percent at the same time last year.

Among metro areas with sufficient data to analyze, the markets with the highest share of lender-owned sales were New Orleans, LA (4.9 percent); St. Louis, MO (4.8 percent); Baton Rouge, LA (4.6 percent); Chicago, IL (4.4 percent); and Davenport, IA (4.4 percent).

The metros with the smallest share of lender-owned sales were Los Angeles, CA (0.6 percent); Las Vegas, NV (0.8 percent); Seattle, WA (0.8 percent); Denver, CO (0.8 percent); and Phoenix, AZ (0.9 percent)

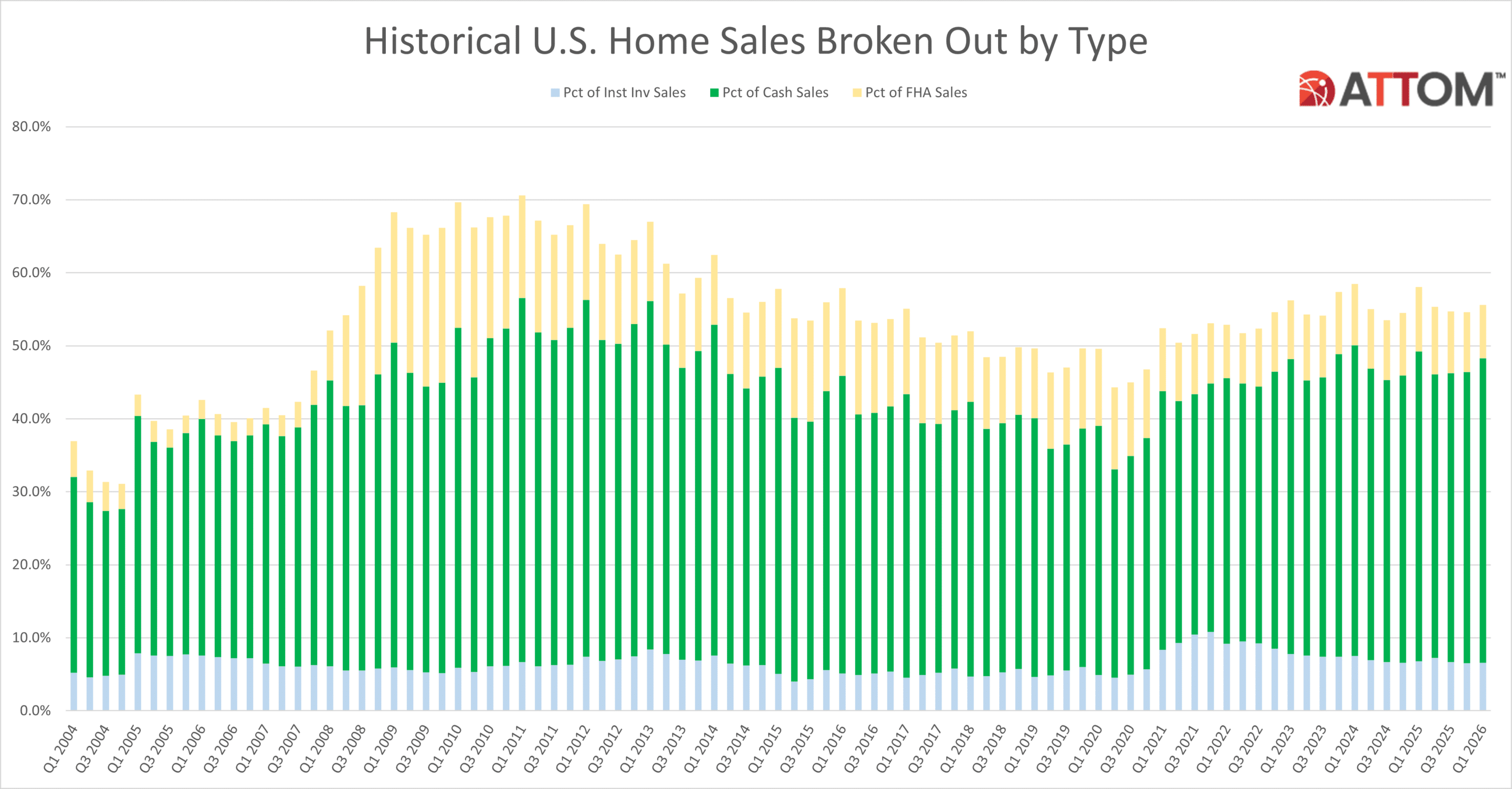

All-cash transactions down year-over-year

Nationwide, 41.7 percent of home sales were completed in all-cash transactions, down from 42.4 percent at the same time last year.

Among metros with sufficient data to analyze for the first quarter of 2026, the markets with the highest rates of all-cash sales (as a percentage of total sales) were Honolulu, HI (76.5 percent); Hilo, HI (74.2 percent); Athens, GA (67.6 percent); Naples, FL (66.6 percent); and Utica, NY (61.6 percent).

The metros with the smallest shares of all-cash sales were Vallejo, CA (23.2 percent); Bremerton, WA (23.3 percent); Olympia, WA (23.7 percent); Kennewick, WA (24.7 percent); and Cedar Rapids, IA (25.1 percent).

Institutional buyers scoop up smaller share of homes

In the first quarter of 2026, homes sold to institutional investors accounted for 6.6 percent of all homes sold nationwide, down from 6.8 percent at the same time last year.

The metro areas with the largest shares of homes sold to institutional investors (as a percentage of all sales) were Mobile, AL (15 percent); Memphis, TN (14.8 percent); Boise City, ID (14.4 percent); Salisbury, MD (13.4 percent); and Huntsville, AL (12.4 percent).

The metros with the smallest shares of homes sold to institutional investors were Honolulu, HI (2.4 percent); Naples, FL (2.7 percent); New Orleans, LA (3.1 percent); Providence, RI (3.1 percent); and New York, NY (3.3 percent).

FHA-backed purchases at four-year low

Buyers using Federal Housing Administration loans purchased 7.4 percent of all homes sold nationwide in the first quarter of 2026, the lowest rate since the second quarter of 2022.

The metro areas with the highest proportion of sales involving FHA loans were Merced, CA (24.9 percent); Laredo, TX (21.8 percent); Visalia, CA (20.3 percent); Bakersfield, CA (19.7 percent); and Modesto, CA (17.9 percent).

Conclusion

Seller profit margins fell in the first quarter of 2026 as mortgage rates rose and home prices held steady after several quarters of record-breaking growth. While typical returns on home sales have continued to trend downward from their 2022 peak, they remain well above pre-pandemic levels, indicating that the market is normalizing but still historically strong.

Report methodology

The ATTOM U.S. Home Sales Report provides percentages of REO sales and all sales that are sold to institutional investors and cash buyers, at the state and metropolitan statistical area. Data is also available at the county and zip code level, upon request. The data is derived from recorded sales deeds, foreclosure filings and loan data. Statistics for previous quarters are revised when each new report is issued as more deed data becomes available.

Definitions

All-cash purchase: sale where no loan is recorded at the time of sale and where ATTOM has coverage of loan data.

Homeownership tenure: for a given market and given quarter, the average time between the most recent sale date and the previous sale date, expressed in years.

Home seller price gains: the difference between the median sales price of homes in a given market in a given quarter and the median sales price of the previous sale of those same homes, expressed both in a dollar amount and as a percentage of the previous median sales price.

Institutional investor purchases: residential property sales to non-lending entities that purchased at least 10 properties in a calendar year.

REO sale: a sale of a property that occurs while the property is actively bank owned (REO).

About ATTOM

ATTOM delivers AI-driven property intelligence built on one of the nation's most trusted property data assets, covering 160 million U.S. properties—99% of the population. Our engineered, multi-sourced real estate data spans property tax, deeds, mortgages, foreclosure, environmental risk, property conditions, natural hazards, neighborhood insights, and geospatial boundaries, rigorously validated for advanced analytics. ATTOM supports analytics and AI-driven applications through flexible delivery options including APIs, bulk licensing, cloud delivery, and the MCP Server for AI-powered, agentic access to engineered property data—enabling organizations to automate analysis and scale property intelligence across industries.

Media Contact:

Megan Hunt

megan.hunt@attomdata.com

Data and Report Licensing:

datareports@attomdata.com