Overall Residential Lending Activity Down Annually by 32 Percent, Marking Fastest Decline in Eight Years; Number of New Loans Decreases for Fourth Straight Quarter; Refinance Lending Drops Another 22 Percent While Purchase Mortgages Dip 18 Percent

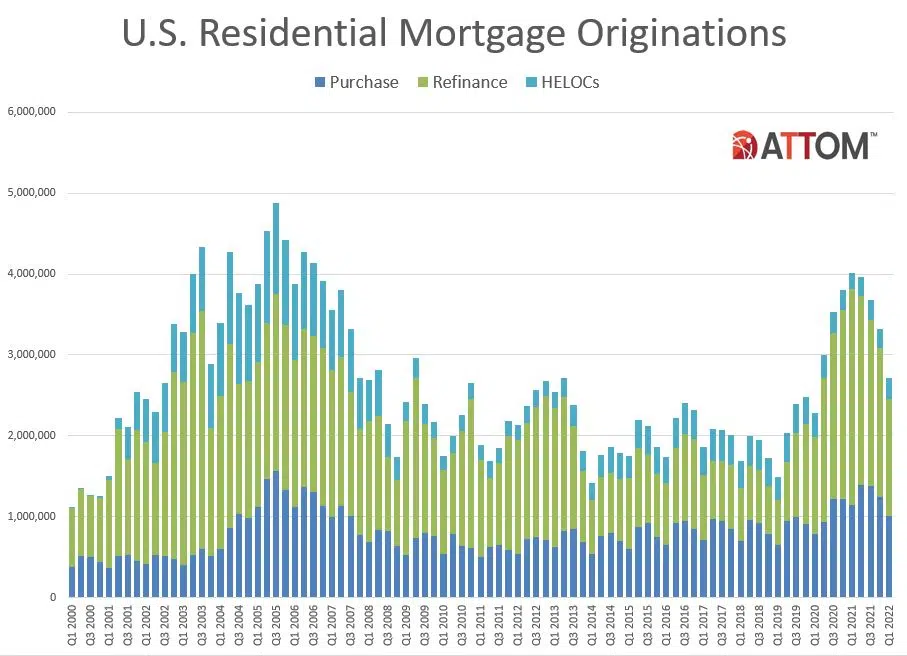

IRVINE, Calif. – June 9, 2022 — ATTOM, a leading curator of real estate data nationwide for land and property data, today released its first-quarter 2022 U.S. Residential Property Mortgage Origination Report, which shows that 2.71 million mortgages secured by residential property (1 to 4 units) were originated in the first quarter of 2022 in the United States. That figure was down 18 percent from the fourth quarter of 2021 – the largest quarterly decrease since 2017 – and down 32 percent from the first quarter of 2021 – the biggest annual drop since 2014.

The decline, which marked the fourth straight quarterly decrease, resulted from double-digit downturns in purchase and refinance activity, even as home-equity lending rose.

Overall, lenders issued $892.4 billion worth of mortgages in the first quarter of 2022. That was down quarterly by 17 percent and annually by 27 percent. As with the number of loans, the quarterly and annual decreases in the dollar volume of loans were the largest in five and eight years, respectively.

The biggest contributor to the downturn was a decrease in refinance deals. Just 1.45 million residential loans were rolled over into new mortgages during the first quarter of 2022, down 22 percent from the fourth quarter of 2021 and 46 percent from a year earlier. Amid rising mortgage interest rates, the number of refinance mortgages decreased for the fourth straight quarter while the annual drop was the largest since 2014. The dollar volume of refinance loans was down 20 percent from the prior quarter and 42 percent annually, to $470.7 billion.

Refinancing, while still a majority of residential lending activity, also decreased again as a portion of all loans during the first quarter of 2022. They represented 53 percent of all first-quarter mortgages, down from 56 percent in the fourth quarter of 2021 and 67 percent in the first quarter of 2021.

“The drop-off in Q1 refinancing activity is no surprise with mortgage rates rising as rapidly as they have,” said Rick Sharga, executive vice president of market intelligence at ATTOM. “But many forecasts expected purchase loans to remain strong in 2022, and even increase in both the number of loans originated and the dollar volume of those loans. The weakness in purchase loan activity shows just how much of an impact the combination of escalating home prices and rising interest rates have had on borrower activity this year.”

Purchase-loan activity shrank in the first quarter of 2022 as lenders issued 1.01 million mortgages to buyers. That tally was down 18 percent quarterly and 12 percent annually. The dollar value of loans taken out to buy residential properties dipped to $371.3 billion, down 16 percent from the fourth quarter of last year and 1 percent from the first quarter of 2021. Despite those decreases, purchase loans remained at 37 percent of all loans in the first quarter of 2022 and were still up annually from 29 percent.

In the one category that bucked the trend, home-equity lending went up 6 percent quarterly and 28 percent annually, to 249,900. So-called HELOC mortgages represented 9 percent of all first-quarter residential loans, up from 7 percent in the fourth quarter of 2021 and 5 percent in the first quarter of last year.

The continued shrinkage in overall residential lending during the first quarter reinforced a stark reversal for the mortgage industry following a near-tripling of activity from early 2019 through early 2021. The first-quarter figures come amid multiple forces that threaten to continue the recent trends, including 30-year mortgage rates that have risen past 5 percent this year, an ongoing tight supply of homes for sale around the country that limits the number of home purchases, rising inflation and other uncertainties surrounding the U.S. economy.

They also add to a list of indicators showing that the nation’s decade-long housing market boom may be cooling off, including slower price growth, smaller home-seller profits and declining home affordability.

Total mortgages drop at fastest pace in five years

Banks and other lenders issued 2,708,492 residential mortgages in the first quarter of 2022. That was down 18.4 percent from 3,320,689 in the fourth quarter of 2021 and down 32.5 percent from 4,011,939 in the first quarter of 2021. The quarterly decline was the largest since the first quarter of 2017, while the annual decrease was the biggest since the second quarter of 2014. The $892.4 billion dollar volume of loans in the first quarter was down 17.1 percent from $1.08 trillion in the prior quarter and was 27.3 percent less than the $1.23 trillion lent in the first quarter of 2021.

Overall lending activity decreased from the fourth quarter of 2021 to the first quarter of 2022 in 213, or 99 percent, of the 216 metropolitan statistical areas around the U.S. with a population of more than 200,000 and at least 1,000 total residential mortgages issued in the first quarter of 2022. Total lending activity was down at least 10 percent in 183 metros (85 percent) and by at least 20 percent in 90 metros (42 percent). The largest quarterly decreases were in Huntsville, AL (down 62 percent); St. Louis, MO (down 52.2 percent); Augusta, GA (down 40.8 percent); Montgomery, AL (down 37.4 percent) and Des Moines, IA (down 35.8 percent).

Aside from St. Louis, metro areas with a population of least 1 million that had the biggest decreases in total loans from the fourth quarter of 2021 to the first quarter of 2022 were San Jose, CA (down 34.1 percent); Boston, MA (down 31.5 percent); Minneapolis, MN (down 30.4 percent) and Rochester, NY (down 29.6 percent).

The only metro areas with increases in the total number of mortgages from the fourth quarter to the first quarter were Philadelphia, PA (up 11.4 percent); Laredo, TX (up 9 percent) and Sioux Falls, SD (up 7.6 percent).

Refinance mortgage originations down 22 percent from fourth quarter

Lenders issued 1,446,622 residential refinance mortgages in the first quarter of 2022, down 21.7 percent from 1,846,450 in fourth quarter of 2021 and down 45.8 percent from 2,670,304 in the first quarter of 2021. The total was down for the fourth straight quarter, which had not happened since late 2013 into early 2014. The $470.7 billion dollar volume of refinance packages in the first quarter of 2022 was down 19.9 percent from $587.5 billion in the prior quarter and down 42.1 percent from $813.1 billion in the first quarter of 2021.

Refinancing activity decreased from the fourth quarter of 2021 to the first quarter of 2022 in 210, or 97 percent, of the 216 metropolitan statistical areas around the country with enough data to analyze. Activity dropped at least 10 percent in 193 metro areas (89 percent) and by at least 20 percent in 109 metros (50 percent). The largest quarterly decreases were in Huntsville, AL (down 58.1 percent); St. Louis, MO (down 49.8 percent); Augusta, GA (down 47.5 percent); Anchorage, AK (down 45.1 percent) and San Jose, CA (down 41.9 percent).

Aside from St. Louis and San Jose, metro areas with a population of least 1 million that had the biggest decreases in refinance activity from the fourth quarter of last year to the first quarter of this year were San Francisco, CA (down 36.7 percent); San Diego, CA (down 35.9 percent) and Boston, MA (down 34.4 percent).

Counter to the national trend, metro areas with the biggest increases in refinancing loans from the fourth quarter to the first quarter were Philadelphia, PA (up 7.8 percent); Macon, GA (up 4.6 percent); Laredo, TX (up 4.5 percent); Lexington, KY (up 3.9 percent) and Beaumont, TX (up 3.2 percent).

Purchase originations decrease 18 percent in first quarter

Lenders originated 1,011,975 purchase mortgages in the first quarter of 2022. That was down 18.3 percent from 1,238,432 in the fourth quarter and down 11.7 percent from 1,145,767 in the first quarter of 2021. The $371.3 billion dollar volume of purchase loans in the first quarter of 2022 was down 16.2 percent from $443 billion in the prior quarter, although off just 0.8 percent from $374.4 billion a year earlier.

Residential purchase-mortgage originations decreased from the fourth quarter of 2021 to the first quarter of 2022 in 205 of the 216 metro areas in the report (95 percent). Loans issued to buyers dropped at least 10 percent in 169 metro areas (78 percent) and by at least 20 percent in 113 metros (52 percent).

The largest quarterly decreases were in Huntsville, AL (down 61.3 percent); St. Louis, MO (down 55.3 percent); Utica, NY (down 50.7 percent); Lafayette, IN (down 50 percent) and Duluth, MN (down 45.9 percent).

Aside from St. Louis, metro areas with a population of at least 1 million that saw the biggest quarterly decreases in purchase originations in the first quarter of 2022 were Rochester, NY (down 40.8 percent); Boston, MA (down 34.8 percent); Honolulu, HI (down 32.2 percent) and San Jose, CA (down 32.2 percent).

Residential purchase-mortgage lending increased from the fourth quarter of 2021 to the first quarter of 2022 in just 11 of the metro areas reviewed (5 percent). The largest increases included Lafayette, LA (up 16.7 percent); Laredo, TX (up 16.5 percent); College Station, TX (up 16.2 percent); Philadelphia, PA (up 12.8 percent) and Warner Robins, GA (up 12.2 percent).

Aside from Philadelphia, the only metro area with a population of at least 1 million where purchase originations increased from the fourth to the first quarter was Houston, TX (up 2.1 percent).

HELOC lending up 6 percent

A total of 249,895 home-equity lines of credit (HELOCs) were originated on residential properties in the first quarter of 2022, up 6 percent from 235,807 during the prior quarter and up 27.6 percent from 195,868 in the first quarter of 2021. HELOC activity increased for the third time in four quarters after decreasing in each of the prior six quarters. HELOCs comprised 9.2 percent of all first quarter-2022 loans, nearly double the 4.9 percent level from a year earlier. The $50.4 billion first-quarter 2022 volume of HELOC loans was up 8.2 percent from $46.6 billion in the fourth quarter of 2021 and 26.3 percent from $39.9 billion the first quarter of last year.

“With affordability apparently slowing down demand from move-up homebuyers, we’re likely to see a continuing increase in HELOCs and cash-out refinance loans, as those homeowners tap into the record $27 trillion of equity to make improvements in their current properties,” Sharga added.

HELOC mortgage originations increased from the fourth quarter of 2021 to the first quarter of 2022 in 62 percent of the metro areas analyzed. The largest increases in metro areas with a population of at least 1 million were in Philadelphia, PA (up 26.4 percent); San Jose, CA (up 23.7 percent); Los Angeles, CA (up 23 percent); Miami, FL (up 22.1 percent) and San Antonio, TX (up 19.6 percent).

The biggest quarterly decreases in HELOCs among metro areas with a population of at least 1 million were in St. Louis, MO (down 51.7 percent); Rochester, NY (down 21.4 percent); Oklahoma City, OK (down 12.8 percent); Memphis, TN (down 10.6 percent) and Providence, RI (down 9.8 percent).

FHA loan portion up again while VA share declines

Mortgages backed by the Federal Housing Administration (FHA) rose as a portion of all lending for the third time in the last four quarters, accounting for 281,306, or 10.4 percent, of all residential property loans originated in the first quarter of 2022. That was up from 9.8 percent in the fourth quarter of 2021 and from 8.9 percent in the first quarter of 2021.

Residential loans backed by the U.S. Department of Veterans Affairs (VA) accounted for 152,733, or 5.6 percent, of all residential property loans originated in the first quarter of 2022, down from 6 percent in the previous quarter and 8.4 percent a year earlier. VA lending as a portion of all loans dropped for the sixth straight quarter.

Median down payments drop slightly even as loan amounts increase

The national median down payment on homes purchased with financing again decreased slightly during the first quarter of 2022, the second straight quarterly drop-off, while the typical amount borrowed rose for the fourth quarter in a row, to another new high. At the same time, the ratio of median down payments to home prices also inched downward.

The median down payment on single-family homes and condos purchased with financing in the first quarter of 2022 was $25,200, down 3.1 percent from $26,000 in the previous quarter but still up 24.4 percent from $20,250 in the first quarter of 2021. Among homes purchased with financing in the first quarter of 2022, the median loan amount was $295,075. That was up 0.7 percent from the prior quarter and up 11 percent from the same period in 2021.

Amid those shifts, the typical down payment was 7.2 percent of the purchase price, down from 7.4 percent in the fourth quarter of 2021.

Report methodology

ATTOM analyzed recorded mortgage and deed of trust data for single-family homes, condos, town homes and multi-family properties of two to four units for this report. Each recorded mortgage or deed of trust was counted as a separate loan origination. Dollar volume was calculated by multiplying the total number of loan originations by the average loan amount for those loan originations.

About ATTOM

ATTOM delivers AI-driven property intelligence built on one of the nation's most trusted property data assets, covering 160 million U.S. properties—99% of the population. Our engineered, multi-sourced real estate data spans property tax, deeds, mortgages, foreclosure, environmental risk, property conditions, natural hazards, neighborhood insights, and geospatial boundaries, rigorously validated for advanced analytics. ATTOM supports analytics and AI-driven applications through flexible delivery options including APIs, bulk licensing, cloud delivery, and the MCP Server for AI-powered, agentic access to engineered property data—enabling organizations to automate analysis and scale property intelligence across industries.

Media Contact:

Christine Stricker

949.748.8428

christine.stricker@attomdata.com

Data and Report Licensing: