From the November/December 2022 issue of the Housing News Report

After a decade of low interest rates and rising home values, 2022 was a year of transition, a time when home sales sank, mortgage costs soared, and affordability slumped. And yet, 2022 also had a number of surprisingly strong fundamentals.

- The rate of real estate appreciation declined, but home values rose.

- Mortgage rates more than doubled, but remained lower than long-term averages.

- Sale activity tumbled, but monthly inventory levels increased.

These 2022 changes are interconnected, and they suggest what’s likely in 2023.

2022 Mortgage Rates

The bloom came off the financial rose in 2022. Weekly mortgage rates more than doubled, going from 3.22% at the start of January to 6.7% at the end of September, according to Freddie Mac.

As rates increased, so did monthly costs. A house that needed $400,000 in financing in January at 3.22% meant the borrower was paying $1,734 per month for principal and interest. Later in the year, in September, the borrower likely borrowed $431,000 to keep up with rising prices. The monthly cost for principal and interest at 6.7% was $2,781 – more than $1,000 extra per month extra.

The real estate marketplace has long functioned with rates at 6.7% and higher. In fact, 6.7% is actually “low” by historic norms. A look at Freddie Mac figures between 1971 and the end of 2021 – a period of 50 years – shows that the average mortgage rate was 7.8%. (The highest annual rate was 16.63% in 1981.)

2023 Mortgage Rates

It turns out that today’s interest rates are quite tolerable for a large portion of the population. This explains why sale prices have been rising and bidding wars are common. Indeed, according to Redfin, nearly 45% of the purchase orders they wrote in August involved one or more competing buyers.

Inflation is a large and potentially destabilizing economic problem. The Fed is working to get the inflation rate down to 2% or so, and one big tool is its ability to raise the federal funds rate, the rate banks pay to borrow money overnight.

While the Fed does not set mortgage rates, it influences them by moving the federal funds rate up and down. Thus, if inflation starts to ease and the Fed stops pushing bank costs higher, we could see stable and perhaps even lower mortgage rates.

While falling mortgage rates in 2023 might seem unlikely, the economy has vast sums of largely unused capital, money that can lead to lower rates. For instance, commercial bank deposits grew by $4.8 trillion between January 2020 and mid-September 2022. Lower rates can lead to more affordability, additional sales, and — with more buyers in the market – higher residential prices.

The Fed to this point has given no hint of a policy slowdown, much less a reversal. As Fed Vice Chair Lael Brainard said in late September, “we are in this for as long as it takes to get inflation down. So far, we have expeditiously raised the policy rate to the peak of the previous cycle, and the policy rate will need to rise further.”

What if the Fed pushes rates too high? Can that lead to steep unemployment levels and an outright recession? That’s a real worry and something to watch, especially when you consider that the economy is huge, difficult to moderate, and subject to outside events such as the war in Ukraine, changing gas prices, and the latest pandemic developments.

Home Prices Up, Down & In Flux

The natural expectation is that skyrocketing mortgage rates will cause home values to tank. But – surprise, surprise – what has happened so far was largely unforeseen.

Existing home sales in August were 19.9% lower than a year earlier, according to the National Association of Realtors (NAR). During the same one-year period, home prices rose 7.7%, marking “126 consecutive months of year-over-year increases, the longest-running streak on record.”

It’s true that August 2022 national prices were higher than a year earlier. And yes, on a year-over-year basis, there has been a decade-long streak of nationwide price increases.

However, it’s equally true that the median August sale price of $389,500 was plainly lower than the $413,800 record high reported in June.

In addition, location counts. As of mid-2022, according to NAR, quarterly San Antonio prices were up 22% while home values in Trenton fell 0.7%. No doubt 2023 price changes will be equally localized.

Affordability Remains Elusive

What we’re seeing in 2022 – at least through September – are generally rising values, but values that are not growing as quickly as they once did. In other words, the pace has slowed. The 7.7% annual appreciation seen in 2022 is perfectly good, but a far cry from the 12.9% growth for 2020 or the 15.4% recorded in 2021.

Even with reduced levels of real estate appreciation, home values have continued to rise, in many cases faster than household incomes. Recent household incomes have actually fallen, going from $72,808 in 2019 to $70,784 in 2021. The result is less affordability for millions of potential buyers.

“Homeownership remains largely unaffordable for the majority of homebuyers in the majority of markets across the country,” said Rick Sharga, executive vice president of market intelligence at ATTOM.

Speaking in late September, Sharga added that “while home prices have declined a bit quarter-over-quarter, they’re still higher than they were a year ago, and interest rates have essentially doubled. Many prospective homebuyers simply can’t afford the home they hoped to buy, and in many cases no longer qualify for the mortgage they’d need.”

It seems clear that the huge value increases seen in 2020, 2021, and so far in 2022 will not be repeated in 2023, especially in light of the Fed’s fight against inflation. At the same time, inflated prices mean ownership is out-of-reach in many households.

The Missing Foreclosure Crisis

Governments at the federal, state, and local levels established widespread foreclosure and eviction bans during the worst of the pandemic. With the end of most bans in the summer of 2021 would we soon see a massive number of dislocations? According to the Consumer Financial Protection Bureau (CFBB), “11 million renter and homeowner households were significantly overdue on their regular housing payments as of December 2020, placing them at heightened risk of losing their homes to foreclosure or eviction over the coming months.”

Such forecasts turned out to be off-the-mark in 2021 and 2022. The same is likely to be the story in 2023. Here’s why.

- Evictions and foreclosures are expensive for lenders and property owners, something to be avoided.

- Because home values have increased significantly during the past few years, owners with financial difficulties are generally able to sell and not face foreclosure.

- According to ATTOM, there were 34,501 foreclosure filings in August – default notices, scheduled auctions, and bank repossessions. That’s a year-over-year increase of 118%, but remember that there were few foreclosures or evictions in 2021.

The Long-Term Shortage of Real Estate Inventory

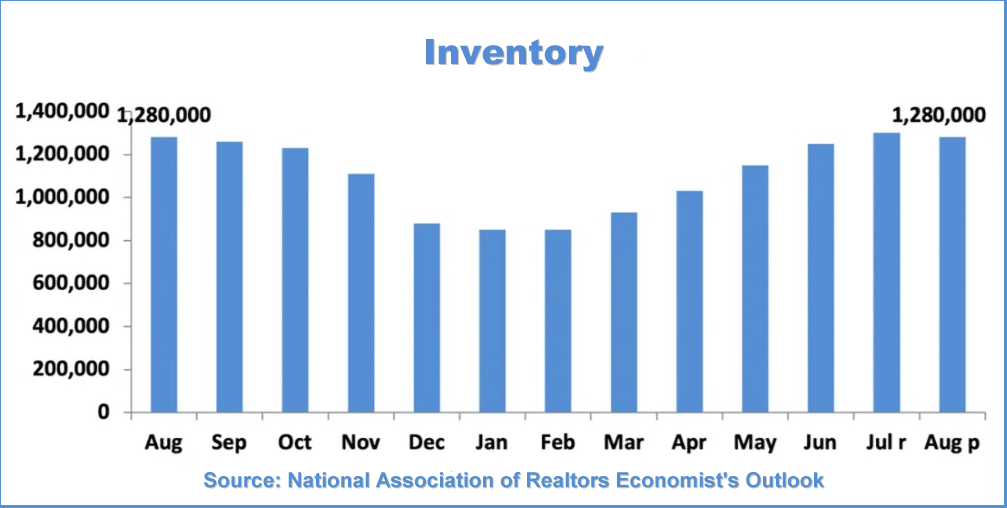

Just about every real estate sales report includes a comment regarding real estate inventory, usually some mention of a shortage and how it would be better if there was a six-month supply of homes for sale.

According to NAR, in August 2021 there was a 2.6 month supply of unsold inventory. In August 2022, inventory amounted to 3.2 months, and yet the number of existing homes available for purchase was the same in both months.

Although the monthly inventory figure has changed, there was no inventory increase, if by “increase” we mean the number of unsold units. Instead, the number of buyers declined, so unsold inventory goes further and will take more months to absorb.

Will there be lots more inventory in 2023? Not likely.

First, those who bought or refinanced during the past few years likely have once-in-a-lifetime mortgage rates that many owners will not want to give up. Stephen Kim and Trey Morrish, analysts with Evercore ISI, pointed out in May 2022 that more than “95% of all outstanding mortgages have fixed terms, and the median rate is <3.4%.”

Second, a replacement property is likely to have both a higher acquisition cost as well as financing with a steeper interest rate. Combine the two, and the resulting cost may not be attractive to sellers, even with proceeds from the sale of a current residence.

Third, we’re not going to build our way out of the inventory shortage, in part because of affordability barriers. In August, the median sale price for a new home was $436,800 versus $389,500 for existing properties. August new home sales were 28.8% below July.

Underbuilding Forces Prices Higher

The ongoing inventory shortage simply adds to the “underbuilding” problem – years of constructing fewer units than population growth and public demand required. How many units are missing? More than five million by some estimates.

A related issue is that we don’t have enough construction workers. In July, the Bureau of Labor Statistics said the building industry had an estimated 375,000 job openings.

Rising interest rates will temper demand and push unit sales lower in 2023, while the lack of inventory will pressure home prices higher. Which force will win out? Most probably, the answer will be decided in the corridors of the Federal Reserve.