Typical Home Sale Nationwide in Second Quarter of 2021 Nets 45 Percent Profit Margin, Down From 48 Percent in Prior Quarter; Decline Marks Rare Dip During Spring Buying Season; Profits Still Well Above 32 Percent Level Seen a Year Ago

IRVINE, Calif. – July 29, 2021 — ATTOM, curator of the nation’s premier property database, today released its second-quarter 2021 U.S. Home Sales Report, which shows that profit margins for home sellers took an unusual dip in the second quarter but still were far above where were they were a year earlier.

In a sign that the housing market remained super-heated but that investment returns may be declining, the report reveals that the typical single-family home and condo sale across the United States during the second quarter of 2021 generated a profit of $94,500. That was up from $90,000 in the first quarter of 2021 and from $60,572 in the second quarter of 2020.

However, the profit margin on the median-priced house or condominium – the return on investment that sellers made on their original purchase price – declined from 48.4 percent in the first quarter of this year to 44.9 percent in the second quarter. While the latest margin remained 13 points above the 32 percent level recorded a year earlier, the drop-off marked a rare decline during a time of year that usually produces some of the best returns for sellers. The last time typical returns on investment dropped nationally during any second-quarter period was in 2008.

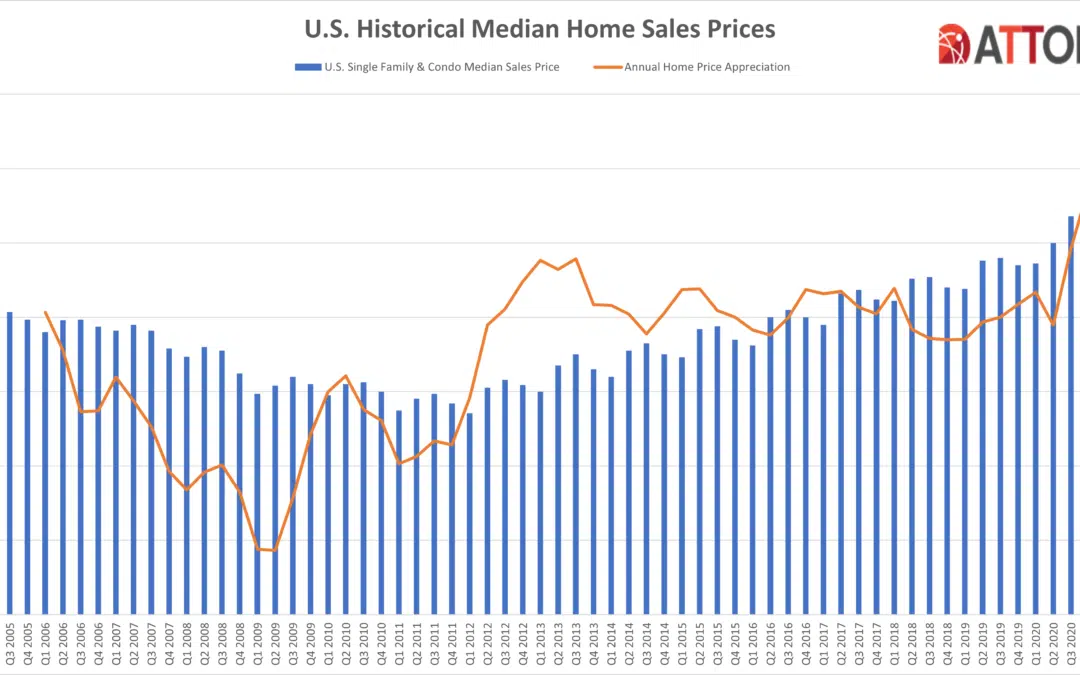

The mixed picture of high, but reduced, profit margins came as the national median home price hit yet another record in the second quarter of 2021, reaching $305,000. That was up 11 percent from $275,200 in the first quarter of 2021 and 22 percent from $250,000 in the second quarter of 2020. The annual price surge marked the largest since at least 2006 and was two to four times greater than increases seen just a year ago.

Still, profits dropped in the second quarter of this year because price gains – high as they were – were smaller than increases that recent sellers had been paying when they originally bought their homes. The gap between the latest price gains and earlier increases caused the dip in profit margins.

While home prices rose from the first to the second quarter of 2021 in 98 percent of U.S. metropolitan areas with enough data to analyze, investment returns rose in only 56 percent.

The recent price and profit trends reflect a housing market that has continued its decade-long upward spiral, even as the Coronavirus pandemic has damaged significant sectors of the U.S. economy since it hit early last year. Amid rock-bottom interest rates and worries about living in congested virus-prone parts of the country, a glut of buyers have been chasing a tight supply of homes for sale, raising demand and spiking prices.

“Prices and profits from the second quarter painted yet another picture of a housing market in high gear – except for one thing. Profit margins dropped in the second quarter, which is very unusual for any Springtime period because that’s when the housing market is usually hottest or close to it,” said Todd Teta, chief product officer at ATTOM. “While it may just be a momentary thing in today’s volatile market, it’s definitely something to keep an eye on in case it’s a sign that the market is finally cooling or giving in to some of the economic forces connected to the virus pandemic.”

Profit margins rise annually in more than 80 percent of metro areas around the U.S. and quarterly in slightly more than half

Typical profit margins – the percent change between median purchase and resale prices – rose from

the second quarter of 2020 to the second quarter of 2021 in 158 (81 percent) of 195 metro areas around the United States with sufficient data to analyze. But margins increased from the first to the second quarter of 2021 in just 109 (56 percent). Metro areas were included if they had at least 1,000 single-family home sales in the second quarter of 2021 and a population of at least 200,000.

The biggest annual increases in profit margins came in the metro areas of Boise City, ID (margin up from 59.6 percent in the second quarter of 2020 to 124.3 percent in the second quarter of 2021); Charlottesville, VA (up from 20.2 percent to 83.6 percent); Scranton, PA (up from 34.9 percent to 80.9 percent); Claremont-Lebanon, NH (up from 18 percent to 57.3 percent) and Bellingham, WA (up from 60.8 percent to 98 percent).

The biggest annual profit-margin increases in metro areas with a population of at least 1 million were in Rochester, NY (margin up from 31 percent to 64.8 percent); Detroit, MI (up from 36.7 percent to 64.4 percent); Indianapolis, IN (up from 40.3 percent to 59.6 percent); Atlanta, GA (up from 32.4 percent to 51.6 percent) and Washington, DC (up from 24.5 percent to 43.5 percent).

From quarter to quarter, the biggest gains among metro areas were in Charlottesville, VA (margin up from 34.2 percent in the first quarter of 2021 to 83.6 percent in the second quarter); Rochester, NY (up from 30.8 percent to 64.8 percent); Charleston, SC (up from 29.2 percent to 57.1 percent); Scranton, PA (up from 55 percent to 80.9 percent) and Claremont-Lebanon, NH (up from 35.7 percent to 57.3 percent).

Profit margins dropped, year over year, in just 37 of the 195 metro areas analyzed (19 percent) but declined quarterly in 86 (44 percent). The biggest annual decreases were in San Jose, CA (margin down from 85.6 percent in the second quarter of 2020 to 67.4 percent in the second quarter of 2021); Las Vegas, NV (down from 45.8 percent to 30.5 percent); Kansas City, MO (down from 41.4 percent to 26.5 percent); Myrtle Beach, SC (down from 26.6 percent to 11.7 percent) and Los Angeles, CA (down from 55.7 percent to 41.3 percent).

Aside from San Jose, Las Vegas, Kansas City and Los Angeles, the largest annual drop in profit margins among metro areas with a population of at least 1 million came in New York, NY (down from 35.7 percent to 25.6 percent).

The biggest quarterly decreases among metro areas were in Macon, GA (margin down from 73.5 percent in the first quarter of 2021 to 33.4 percent in the second quarter); Bremerton, WA (down from 83.8 percent to 48.4 percent); Lakeland, FL (down from 52.7 percent to 27.6 percent); San Jose, CA (down from 91.7 percent to 67.4 percent) and Stockton, CA (down from 96 percent to 73.2 percent).

Western metros continue to have highest profit margins; southern metros have smallest

The West continued to have the largest profit margins on typical home sales around the country, with 12 of the top 15 returns on investment in the second quarter of 2021 from among the 195 metropolitan areas with enough data to analyze. They were led by Boise City, ID (124.3 percent return); Bellingham, WA (98 percent); Spokane, WA (84.2 percent); Salem, OR (84 percent) and Charlottesville, VA (83.6 percent).

Thirteen of the 20 smallest margins were in the South region. The lowest were in Columbus, GA (minus 5.8 percent); Shreveport, LA (3.6 percent); Lafayette, LA (8.1 percent); Rockford, IL (11.4 percent) and Myrtle Beach, SC (11.7 percent).

Prices up in almost every metro area

Median home prices in the second quarter of 2021 exceeded values from a year earlier in 97 percent of metropolitan statistical areas with enough data to analyze. Nationally, the median price of $305,000 in the second quarter was up 10.8 percent from $275,200 in the first quarter of 2021 and 22 percent from $250,000 in the second quarter of last year.

The biggest year-over-year increases in median home prices during the second quarter of 2021 came in Barnstable Town, MA (up 53 percent); East Stroudsburg, PA (up 46 percent); Worcester, MA (up 42 percent); Dover, DE (up 38 percent) and Brunswick, GA (up 34 percent).

The largest annual increases in metro areas with a population of at least 1 million in the second quarter of 2021 were in Boston, MA (up 27 percent); Austin, TX (up 26 percent); Seattle, WA (up 25 percent); Nashville, TN (up 24 percent) and Tampa, FL (up 24 percent).

Home prices in the second quarter of 2021 hit or tied all-time highs in 82 percent of the metro areas in the report, including New York, NY; Los Angeles, CA; Chicago, IL; Dallas, TX, and Houston, TX.

The largest year-over-year decreases in median prices during the second quarter of 2021 were in Lynchburg, VA (down 6 percent); Pittsburgh, PA (down 6 percent); Peoria, IL (down 2 percent); Fort Wayne, IN (down 2 percent) and Lansing, MI (down 1 percent).

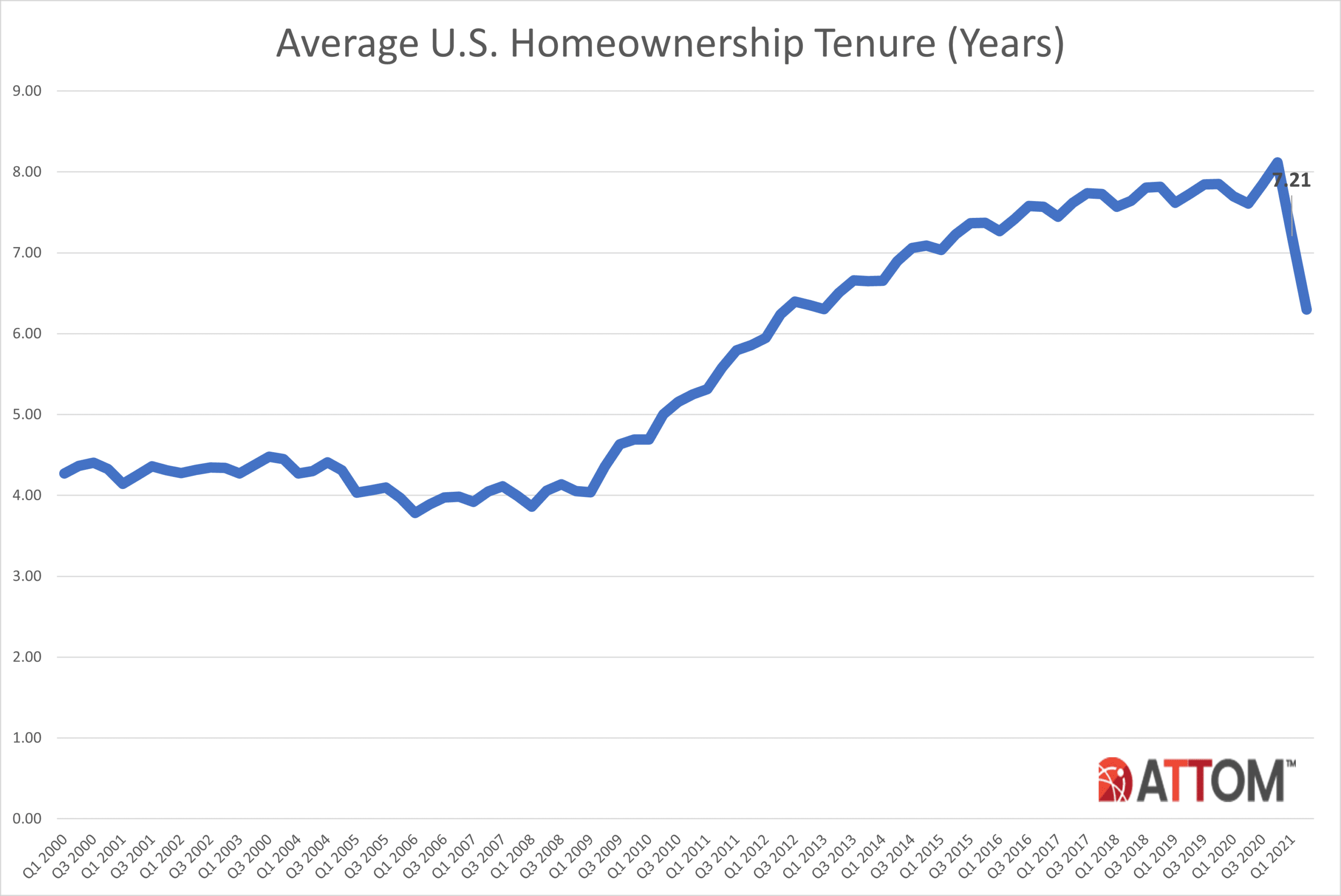

Homeownership tenure falls to 8-year low

Homeowners who sold in the second quarter of 2021 had owned their homes an average of 6.3 years, down from 7.21 years in the first quarter of 2021 and from 7.61 years in the second quarter of 2020. The latest average tenure figure marked the shortest time between purchase and resale since the first quarter of 2013.

Among metro areas with sufficient data, 90 percent saw decreases in average tenure from the second quarter of 2020 to the second quarter of 2021. They were led by Lakeland, FL (tenure down 60 percent); Tucson, AZ (down 53 percent); Norwich, CT (down 43 percent); Memphis, TN (down 42 percent) and Merced, CA (down 42 percent).

Fourteen of the 20 longest average tenures among sellers in the second quarter of 2021 were on the East Coast or West Coast. They were led by Lake Havasu City, NV (11.44 years); Las Vegas, NV (10.86 years); Manchester, NH (10.51 years); Salem, OR (10.44 years) and Yakima, WA (10.13 years).

The smallest tenures during the second quarter of 2021 were in Lakeland, FL (2.96 years); Memphis, TN (4.04 years); Tucson, AZ (4.15 years); Nashville, TN (5.16 years) and Knoxville, TN (5.17 years).

Institutional investment shoots up to nearly a 6-year high

Institutional investors nationwide accounted for 4.6 percent of all single-family house and condo purchases in the second quarter of 2021, the highest level since the fourth quarter of 2015. The latest figure was up from 3.2 percent in the first quarter of 2021 and from 2 percent in the second quarter of last year.

Among states with enough data to analyze, those with the largest percentages of sales to institutional investors in the second quarter of 2021 were Mississippi (11 percent of all sales), Arizona (10.4 percent), Georgia (8.8 percent), Nevada (7.6 percent) and North Carolina (6.7 percent).

States with the smallest levels of sales to institutional investors in the second quarter of 2021 were New Hampshire (1.2 percent), Rhode Island (1.3 percent), Massachusetts (1.5 percent), Hawaii (1.5 percent), and Louisiana (1.6 percent).

Cash sales up to six-year high

Nationwide, all-cash purchases accounted for 34 percent of all single-family house and condo sales in the second quarter of 2021, the highest level since the first quarter of 2015. The second-quarter 2021 number was up from 31.7 percent in the first quarter of 2021 and from 20.6 percent in the second quarter of last year.

Those metros where cash sales represented the smallest share of all transactions in the second quarter of 2021 included Myrtle Beach, SC (8.3 percent of all sales); Lexington, KY (16.5 percent); Washington, DC (16.7 percent); Salem, OR (16.8 percent) and Lincoln, NE (17.6 percent).

FHA-financed purchases at nearly 14-year low

Nationwide, buyers using Federal Housing Administration (FHA) loans accounted for only 7.9 percent of all single-family home purchases in the second quarter of 2021, the lowest level since the fourth quarter of 2007. The latest figure was down from 9.1 percent in the previous quarter and from 12.9 percent a year earlier.

Among metropolitan statistical areas with a population of at least 200,000 and sufficient FHA-buyer data, those with the highest levels of FHA buyers in the second quarter of 2021 were Lakeland, FL (24.4 percent of all sales); Corpus Christi, TX (21.4 percent); Utica, NY (19.6 percent); Beaumont, TX (18.3 percent) and McAllen, TX (18 percent).

###

Report methodology

The ATTOM U.S. Home Sales Report provides percentages of distressed sales and all sales that are sold to investors, institutional investors and cash buyers, a state and metropolitan statistical area. Data is also available at the county and zip code level upon request. The data is derived from recorded sales deeds, foreclosure filings and loan data. Statistics for previous quarters are revised when each new report is issued as more deed data becomes available.

Definitions

All-cash purchase: sale where no loan is recorded at the time of sale and where ATTOM has coverage of loan data.

Homeownership tenure: for a given market and given quarter, the average time between the most recent sale date and the previous sale date, expressed in years.

Home seller price gains: the difference between the median sales price of homes in a given market in a given quarter and the median sales price of the previous sale of those same homes, expressed both in a dollar amount and as a percentage of the previous median sales price.

Institutional investor purchases: residential property sales to non-lending entities that purchased at least 10 properties in a calendar year.

About ATTOM

ATTOM delivers AI-driven property intelligence built on one of the nation's most trusted property data assets, covering 160 million U.S. properties—99% of the population. Our engineered, multi-sourced real estate data spans property tax, deeds, mortgages, foreclosure, environmental risk, property conditions, natural hazards, neighborhood insights, and geospatial boundaries, rigorously validated for advanced analytics. ATTOM supports analytics and AI-driven applications through flexible delivery options including APIs, bulk licensing, cloud delivery, and the MCP Server for AI-powered, agentic access to engineered property data—enabling organizations to automate analysis and scale property intelligence across industries.

Media Contact:

Christine Stricker

949.748.8428

christine.stricker@attomdata.com

Data and Report Licensing:

949.502.8313