ATTOM’s recently released Q2 2022 U.S. Home Equity and Underwater Report shows that 48.1 percent of mortgaged residential properties in the U.S. were considered equity-rich in Q2 2022. The report noted that figure was up from 44.9 percent in Q1 2022 and 34.4 percent in Q2 2021.

According to the latest home equity and underwater analysis, the latest increase – to virtually half of all mortgage payers – marks the ninth straight quarterly rise in the portion of homes in equity-rich territory. The home equity data report also found that at least half of all mortgage-payers in 18 states were equity-rich in Q2 2022, compared to only three states in Q2 2021.

ATTOM’s home equity and underwater report defines equity-rich properties as those where combined estimated amount of loan balances secured by those properties was no more than 50 percent of their estimated market values.

Also according to the report, across the country, 49 states saw equity-rich levels increase from Q1 2022 to Q2 2022, while seriously underwater percentages dipped in 46 states. The report notes that year over year, equity-rich levels rose in all 50 states and seriously underwater portions dropped in 46 states.

ATTOM’s Q2 2022 analysis also found that seven of the 10 states where the equity-rich share of mortgaged homes increased most from Q1 2022 to Q2 2022 were in the southern region of the U.S., with the biggest increases in: Wyoming, where the portion of mortgaged homes considered equity-rich rose from 26.1 percent in the first quarter to 33.9 percent in the second quarter, Maine (up from 48.5 percent to 56.3 percent), Florida (up from 53.6 percent to 60.4 percent), Mississippi (up from 23.5 percent to 29.1 percent) and South Carolina (up from 41.2 percent to 46.5 percent).

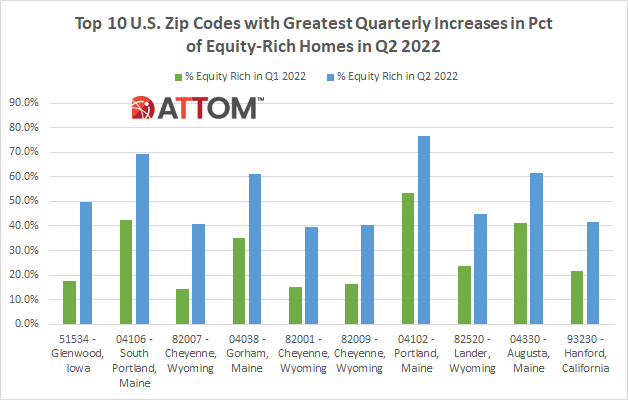

In this post, we dig into the data behind the latest ATTOM home equity and underwater report to uncover the top 10 U.S. zip codes with the greatest quarterly increases in equity-rich properties in Q2 2022. Those zips include: 51534 – Glenwood, Iowa (up from 17.6 percent in Q1 2022 to 49.7 percent in Q2 2022); 04106 – South Portland, Maine (up from 42.3 percent in Q1 2022 to 69.3 percent in Q2 2022); 82007 – Cheyenne, Wyoming (up from 14.1 percent in Q1 2022 to 40.6 percent in Q2 2022); 04038 – Gorham, Maine (up from 35.2 percent in Q1 2022 to 61.3 percent in Q2 2022); 82001 – Cheyenne, Wyoming (up from 15.2 percent in Q1 2022 to 39.8 percent in Q2 2022); 82009 – Cheyenne, Wyoming (up from 16.5 percent in Q1 2022 to 40.3 percent in Q2 2022); 04102 – Portland, Maine (up from 53.5 percent in Q1 2022 to 76.5 percent in Q2 2022); 82520 – Lander, Wyoming (up from 23.6 percent in Q1 2022 to 44.9 percent in Q2 2022); 04330 – Augusta, Maine (up from 41.1 percent in Q1 2022 to 61.4 percent in Q2 2022); and 93230 – Hanford, California (up from 21.5 percent in Q1 2022 to 41.7 percent in Q2 2022).

ATTOM’s latest home equity and underwater report also shows that just 2.9 percent of mortgaged homes, or one in 34, were considered seriously underwater in Q2 2022, with a combined estimated balance of loans secured by the property of at least 25 percent more than the property’s estimated market value. That figure was down from 3.2 percent of all U.S. homes with a mortgage in Q1 2022 and 4.1 percent, or one 24 properties, in Q2 2021.

According to the report, states with the biggest decreases in the percentage of mortgaged homes considered seriously underwater from Q1 2022 to Q2 2022 were spread across the Northeast, South and Midwest, led by: Mississippi (share of mortgaged homes seriously underwater down from 17 percent to 8.1 percent), Wyoming (down from 10 percent to 7 percent), Missouri (down from 6.6 percent to 5.2 percent), Maine (down from 3.1 percent to 2.2 percent) and Connecticut (down from 4 percent to 3.3 percent).

Want to see how your area fares in equity-rich or underwater properties share? Contact us to find out how!