It is said that a rising tide lifts all boats, but what happens when the tide goes out? That’s the big question for 2023, a year when the real estate market is likely to be battered by inflation, steep interest rates, slow sales, and perhaps even a recession.

The case for real estate ownership is compelling even with choppy waters. The Federal Reserve publishes a Survey of Consumer Finances (SCF) every three years and the numbers for 2019 showed that homeowners had a typical net worth of $255,000 versus $6,300 for renters. Given the massive real estate price jumps seen since 2019, the next SCF study is likely to show an even greater disparity when published in September.

And yet, as 2022 serenely sinks below the horizon, we are left with a real estate market that’s in flux. For nearly a decade, rising prices have seemed like a given in most markets. The National Association of Realtors (NAR) reported that November existing home prices marked “129 consecutive months of year-over-year increases, the longest-running streak on record.”

Such steady price gains mean increasing equity as well as a marketplace with little risk for lenders and mortgage insurers, one reason for the low rates seen in recent years.

Steady and widespread price gains also mean something else: Large numbers of owners, loan officers, brokers, and potential buyers have never seen a softening real estate market.

Recent Real Estate Market Trends

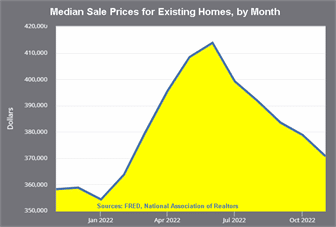

NAR figures show that existing home prices rose 9% in 2019, 12.9% in 2020, and 15.4% in 2021 – a 42% increase in just three years. It’s unrealistic to believe that annual gains at such levels could continue and – sure enough – they didn’t. NAR reported that November existing home values, the latest available at this writing, were up 3.5% from a year earlier.

Did typical property owners really lose $43,100 – 10.42% – in just a few months? Sounds scary, but you can bet that virtually no one who bought for $413,800 in June turned around and sold for $370,700 in November.

Mortgages and Financial Stability

Residential property values have declined on paper more than 10% in recent months, so how has that impacted mortgage borrowers? In terms of existing 30-year mortgages and similar long-term real estate products the reaction has been a big financial shrug.

As long as homeowners keep making their monthly payments, such loans are performing. And most borrowers, to their credit, are making monthly payments.

According to ATTOM Data Solutions, in November just 22 out of every 100,000 housing units were the subject of a foreclosure filing such as a default notice, scheduled auction or bank repossession.

Why Real Estate Will Continue to Sell in 2023

Given slowing sales, iffy prices, and mortgage rates that are likely to rise, why will millions of homes be sold in the coming year?

Inflation. There’s no doubt that rising prices are the financial terror of the moment. Nobody wants excessive inflation, but – like dessert – just enough is generally acceptable and even desirable.

The Federal Reserve is shooting for a 2% inflation rate, a lot less than the 7.1% annual rate seen in November. But even if inflation levels fall to 2% or so, even if a little inflation spurs growth, the cost of goods in cash terms will continue to rise because dollars will buy less and less.

A 2% inflation goal is not a guarantee of rising values for all properties, but in general a little inflation can foster an environment that favors moderately rising prices.

The caution, however, is this: If the Fed pushes interest rates too high in an effort to combat inflation then we might lurch into a recession and – with it a general slowdown – lower wages and higher unemployment.

Population and migration. Our numbers keep going up. We added more than 1.2 million people in 2022. From a 2023 perspective, such numbers mean there’s increased demand, more people to house, and insufficient new construction – the so-called “underbuilding” gap.

However, demand is not uniform. People are moving from state to state. Texas and Florida, with warmer weather and no state income taxes, each gained 400,000 new residents in the past year while New York, California, and Illinois individually lost 100,000 people.

The changing workplace. While a growing population helps maintain real estate demand, we now have a new and uncharted factor to consider: the work-from-home (WFH) movement.

The Census Bureau reports that “between 2019 and 2021, the number of people primarily working from home tripled from 5.7% (roughly 9 million people) to 17.9% (27.6 million people).”

The number of people who work full-time from home will likely decline as the pandemic recedes and employers call workers back to the office while at the same time the number of office employees with flexible schedules will greatly increase from 2019 levels. The result will be more demand for properties with distinct home office spaces.

While the work-from-home movement will create new real estate demand, the exact shape of that demand is unclear. Full-time distant workers, for example, can live wherever they prefer while those with flexible schedules will remain near employment centers. Still, more demand is better for property owners than less demand.

Most property owners, most of the time, are simply marketplace observers. The Census Bureau estimates that we have 142.2 million housing units nationwide. Of this number, 64.6% – 91.86 million – are owner-occupied. The National Association of Realtors expects about 4.1 million home sales in 2022. If that turns out to be the final number, it means roughly 87.8 million homeowners – almost 96% – are on the sidelines.

Most owners didn’t sell when values peaked, so potential “profits” were never banked. Equally important, most property owners do not have an actual “loss” from recent price declines because they didn’t buy at the top of the market.

Equally important, when owners do sell, they will compare their original cost with their sale price and not some mythical value they could have gotten if only they had sold at some point in the past, an action they didn’t take.

The inflation hedge. Rising interest rates are not a worry for most existing property owners. If anything, higher home prices and interest rates simply confirm the original choices to buy and borrow.

Homeowners flooded lender offices when rates were at or near record lows. In May, analysts Stephen Kim and Trey Morrish with Evercore ISI reported that 95% of all outstanding home mortgages were priced at 3.4% or below.

Those with fixed-rate mortgages or who paid cash have seen no increase in monthly mortgage costs, the measure that counts for millions of households. Existing borrowers are generally locked in at the best rates available during the past few years and are simply not in the market to finance or refinance.

In the last week of December, for example, refinancing applications were 87% lower than a year earlier, according to the Mortgage Bankers Association. Purchase financing was down 42% during the same period.

Inventory. Perhaps the foggiest aspect of the 2023 real estate market concerns inventory. In November the number of available homes was up from a year ago, but in November 2021 the inventory supply stood at only 2.1 months.

With higher mortgage rates and less marketplace leverage, owners are hanging on to their properties. As NAR explained in late 2022, “the median expected home tenure for first-time buyers was 18 years, the highest ever recorded and up from 10 years in 2021.”

A new buying opportunity? For the past few years the real estate market has been a seller’s paradise fueled by pandemic fears and historically-low interest rates. At the start of 2023 a new market emerged, one with greater balance between buyers and sellers.

“Home sellers,” said Redfin, “gave concessions to buyers in 41.9% of home sales in the fourth quarter – the highest share of any three-month period in Redfin’s records.”

The company added that “concessions have made a comeback as rising mortgage rates, inflation and economic uncertainty have dampened homebuying demand, giving the buyers who remain in the market increased negotiating power.”

Translation: The days are gone when buyers were widely willing to drop home inspections and other contingencies. Seller contributions will be more common, concessions buried beneath the surface in recorded sale prices.

It’s not a buyer’s market at this writing, but at least purchasers are sensing that some bargaining may be possible. It’s another opportunity to get into the market, one that millions of purchasers will take advantage of during the coming year.